The thing about print adverts was that they stayed where they were. Photo by Bethan on Flickr.

TL:DR: when Apple’s iOS 9 comes out in September, there’s going to be a dramatic uptake of ad blockers on iOS – and it’s going to have far-reaching effects not just on websites and advertisers, but potentially also on the balance in mobile platforms and even on Google’s revenues.

Now, the longer version.

Remember newspapers?

In the old days, adverts appeared in print, on the radio and on the TV. Most ad-supported news organisations that have shifted to the internet began in print.

Ads in print were straightforward. Advertisers bought space, and editors could turn them down, or sometimes decide not to run them if a story broke that would bring about an awkward juxtaposition of, say, the advert for a shoe store on page 3 and the big breaking story now being placed on page 3 about people having feet crushed by a runaway steamroller. (The ad would get moved to another page.) Print ads were hard for advertisers to track, though they could use codes and so on that would clue them in to where someone had seen one if they responded directly.

Then came the internet, and the promise of measuring which adverts people had seen, and which they had clicked, followed swiftly by the realisation that you’d be able to follow what adverts people had seen between different sites by use of tracking cookies and scripts.

Now we have the situation where news websites are plentiful (some just rewriting, sometimes by machine, sometimes not) and adverts even more so: the attempt by The Verge’s Nilay Patel to pin the blame on mobile browsers’ lack of capability has been effectively shot down by Les Orchard, who pointed out the colossal amount of data that a simple page requires.

That’s where we’re at: websites are getting overloaded with ads, beacons, trackers and scripts that are all scrambling over each other in their attempt to squeeze the last bit of information about us from every page.

But nobody asked us, the readers, along the way whether that was OK. And now, people are deciding that it’s not OK.

Block that ad!

The uptake of AdBlock and its commercial sibling Adblock Plus has been gradual, but has now reached more than 150m users, and it’s accelerating. People are getting pissed off with the huge data loads pages impose without their consent, and the idea that they’re being tracked without their consent. In this post-Snowden age, the latter particularly bugs people. Fine, I came to your site; record the fact. But you’re watching me wherever I go online? That’s not acceptable.

People are also pissed off about what can happen when they view an advert online. In all the years I’ve viewed print adverts, I’ve never had one that:

• filled the page I was trying to read and insisted I either wait or click on a particular point on the page to read the article I came for;

• moved up from off the page to insert itself in front of the article I was reading and ask me to sign up for a mailing list;

• started automatically playing a video advert while I was reading some text;

• infected my computer with malware inserted in the ad;

• ran a Javascript script that pretended I need to pay a ransom, or otherwise blocked any interaction unless I pressed a button saying “OK”;

• turned me away from the page I was reading to a completely different one demanding I download an unrelated app.

You may well have other examples. (I’ve not had the malware/Javascript experience online, but other people certainly have.)

Apple: bite me

Into this comes Apple, which guards the user experience on the iOS platform, its biggest moneymaker, very jealously. Apple’s executives and staff aren’t blind to the things that are going on; they use their phones, and they get the same experiences. User experience is what Apple puts above pretty much everything else, and they’ve decided that they don’t like the experience available through the ad-supported web, and so they’re going to do something about it. Hence content blockers for Safari (and all web views) on iOS 9, which wasn’t announced onstage at WWDC but was one of those “Whoa!” moments on browsing through the Settings in the first iOS 9 beta. (Do read the link in the previous sentence, which explains what iOS 9 content blockers are, and are not.) Hence also Apple News, which is basically “all those sites but with the crap taken out”.

The ad intrusion situation on mobile is arguably worse than on desktop, since people are more sensitive about the amount of data they download on mobile, and their phones are less powerful so that complex layouts take longer.

You can get some adblockers for Android (though reviews for the main one are mixed), though you can’t get AdBlock Plus. You can get Ghostery (which shows you what you’re being tracked by) for Android. But there’s nothing like either presently for iOS.

That’s going to change, and I think the advent of iOS 9 and content blocking extensions will touch off a firestorm.

Update: just to clarify: content blocking extensions aren’t built in to iOS 9; only the capability to use them. But people are already working on them. You’ll have to download them and install them, rather like third-party keyboards.

Here’s a video of one presently being developed by Chris Aljoidi:

/Update

These blocking extensions will be paid for (at least initially), but the effect of people tweeting and updating Facebook about how much they enjoy the ad-free web will be hard to ignore. As Carl Howe observes, “Like it or not, once Apple supports ad-blocking in its browsers, it will become the default for people who don’t want tracking.” That also plays into Apple’s other general message, about how it doesn’t track what you do when you’re using its products.

Once this begins happening on mobile, it’s going to sweep back on to the desktop. “How do I do this on my PC?” will become quite a common question. People will load up with adblockers. That’s when websites will begin to face a real problem.

The moral conundrum

Of course, at this point we should step back and ask “why were the adverts there in the first place?” Oh yes, because they help pay for the content. In some – well, many, almost all – cases, they pay for all of the content. As Rene Ritchie of iMore explains, these days sites have to rely on getting ad inventory from all over to fill space; multiple networks vie to fill the space with the most apposite ad for the lowest price (to the advertiser) that the publisher will accept.

It’s worth considering what Ritchie wrote at length:

While we sell premium ads directly to advertisers, that only fills a small subset of the required “inventory” to support the network. Some 85% of ads we served last month were “programmatic”—provided by ad exchanges like Google Adx and Appnexus. Those exchanges are pretty much black boxes. We get a tag, we insert it, and ads appear.

Each ad gets its own iframe, so load is asynchronous and, if one fails, it doesn’t kill the entire site. Unfortunately, that also means each one fires its own trackers, even if those trackers are identical across ads. It’s terribly inefficient.

We’ve tried to find or figure out a way to streamline them, but haven’t been able to. They’re built into the foundations of all the major networks, ad and social, ostensibly to provide more “relevant” content.

When we do get good ads, as soon as they finish their allotted impressions, they go away, and the ad spot gets back-filled with “remnants” which get progressively worse and worse the more we refresh the site.

We also have no ability to screen ad exchange ads ahead of time; we get what they give us. We can and have set policies, for example, to disallow autoplay video or audio ads. But we get them anyway, even from Google. Whether advertisers make mistakes or try to sneak around the restrictions and don’t get caught, we can’t tell. It happens, though, all the time.

So ads are out of control even for sites. That’s so removed from the world of print, where an editor could veto or move an ad, that it’s boggling.

It’s this lack of control – the mad desire and demand by advertisers to get everything, indifferent to the effect of the user experience on the reader – that is driving people to adblockers. It’s a variant of the tragedy of the commons.

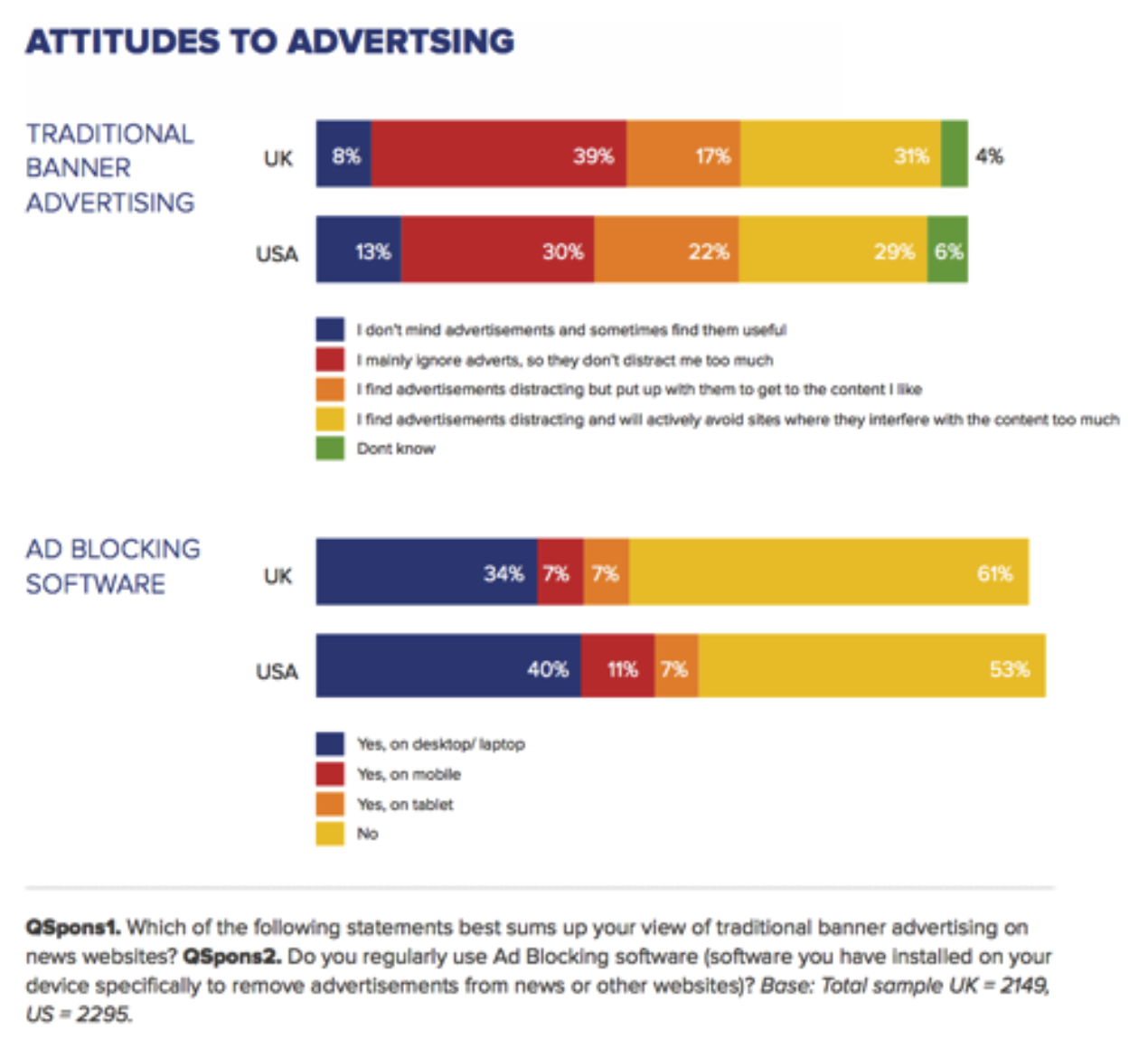

People don’t like it; here’s what a recent survey for Reuters shows. (What it doesn’t show is how many of those who don’t block ads know of the capability for doing it.)

Not very legible; adblocking is the lower bars. People aren’t happy.

But wait, what about the moral dimension? The fact that if you block the ads, the sites lose their income?

I’ve previously written that the two sides on this are far apart; that adblocking is the new speeding: those who do it can justify why to themselves, while those who think it’s wrong are stern in their disapproval.

Entertainingly, when I noted on Twitter how many trackers I’d blocked using Ghostery (as part of an experiment using Ghostery, AdBlock, Javascript Blocker and uBlock to see how it changed my browsing experience), I was at once the object of finger-wagging and the accusation of the destruction of journalism:

@GeorgeBouras @charlesarthur And perhaps be done with quality media and journalism while you're at it. Have you no responsibility to them?

— Jeff Jarvis (@jeffjarvis) July 26, 2015

Have I any responsibility to them? Well, not really. Certainly as a standard reader, here’s what happened: I accepted an invitation to read an article, but I don’t think that we quite got things straight at the top of the page over the extent to which I’d be tracked, and how multiple ad networks would profile me, and suck up my data allowance, and interfere with the reading experience. Don’t I get any say in the last two, at least?

Hence my response:

@jeffjarvis @GeorgeBouras I think it's dangerous to think that readers must, or will, tolerate anything advertisers demand.

— Charles Arthur (@charlesarthur) July 26, 2015

(You can view the entire conversation if you’re logged in to Twitter.)

Print evolved. Now it’s the web advertisers’ turn

This is the part of the debate that so interests (and, frankly, entertains) me. Print-based organisations were told they needed to evolve, and stop being such dinosaurs, because the web was where it was at: advertising was moving, and if they didn’t move too, they’d just die.

Now we’re all online, but somehow we’re meant to accept that web advertising is how it is, and never question or deviate from it? Nuh-uh. Why should web advertisers be immune from evolutionary or revolutionary change in user habits? What’s sauce for the print goose is sauce for the online gander. I don’t recall the people who scolded me for using tracking detectors previously saying that everyone had to stick with print adverts because they made more money (which those ads still do).

Furthermore, any argument that tries to put a moral dam in front of a technological river is doomed. Napster; Bittorrent; now adblocking.

Which quickly leads to…

If any significant number of users shift to using adblockers, web advertisers are going to have to move quickly to deal with that new reality. Web publishers too.

(Though I have to say I have very little sympathy for a lot of web “publishers”. Back in the early days of the web, the Guardian ran a brilliant ad which asked “Ever wondered how every day there’s just enough news to fit in the newspaper?” It was advertising the Guardian website, and the fact there was more there than you’d find in the paper.

Now? There are a gazillion websites – but tons of them are simple copies, monetised by adverts from Google or whoever, which leach from the originating sites by copying their content. We’ve now established the limits of how much news is generated each day: it’s more than fits in newspapers, but less than fits on all the websites currently dedicated to “news”. If adblocking puts some of the copiers on the skids, I won’t weep. That’s not journalism; it’s a sort of horrible stenography, even worse than some of the stenography that does pass for journalism at some bigger sites. Good journalism, and worthwhile sites, will survive. Or good journalists will.)

What form will the evolution take? Well, look at sites like Buzzfeed, and their use of native content. If the site generates the ad, it’s suddenly a lot harder to block. We’re back, in a way, in the land of print, where the printing of the editorial and the ads happened in the same place.

Ecosystem fights

Beyond all this, there’s a longer-term potential effect. I don’t think Apple was gleefully thinking of ways to nobble Google when it decided to introduce content blocking, but this could have quite an effect.

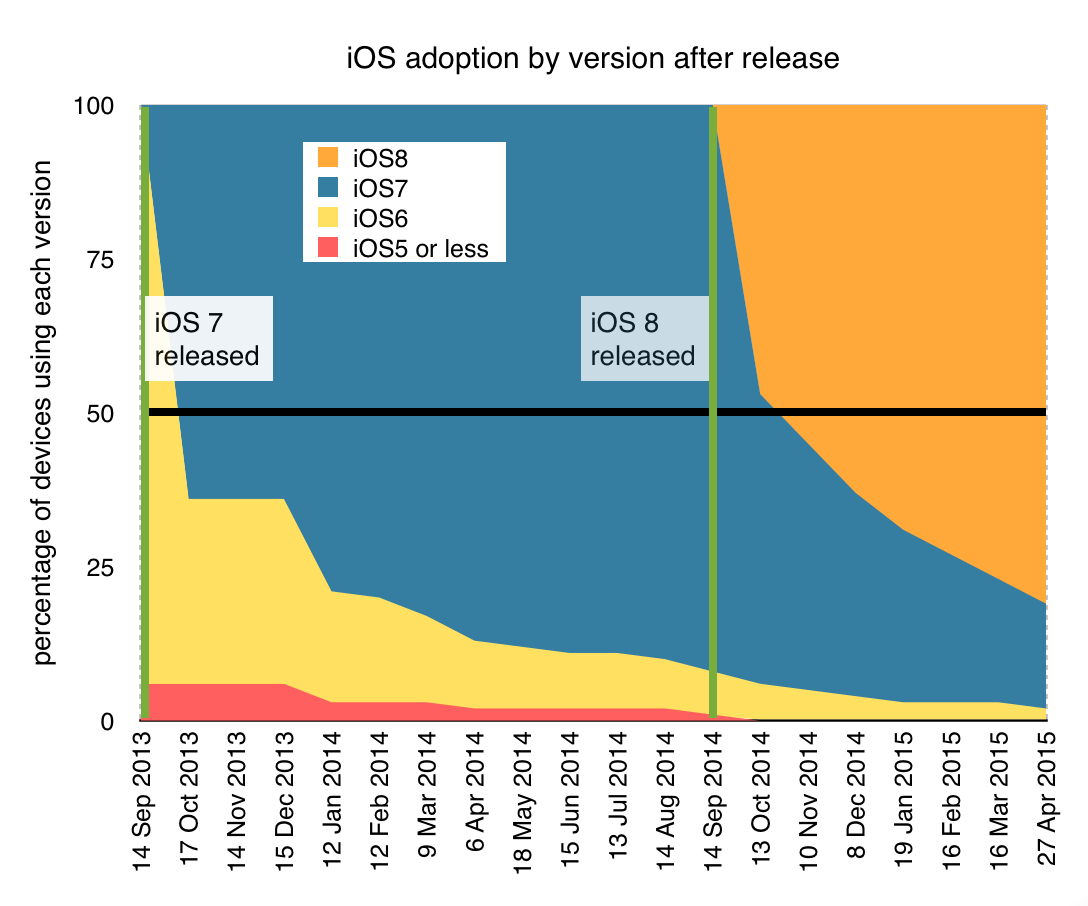

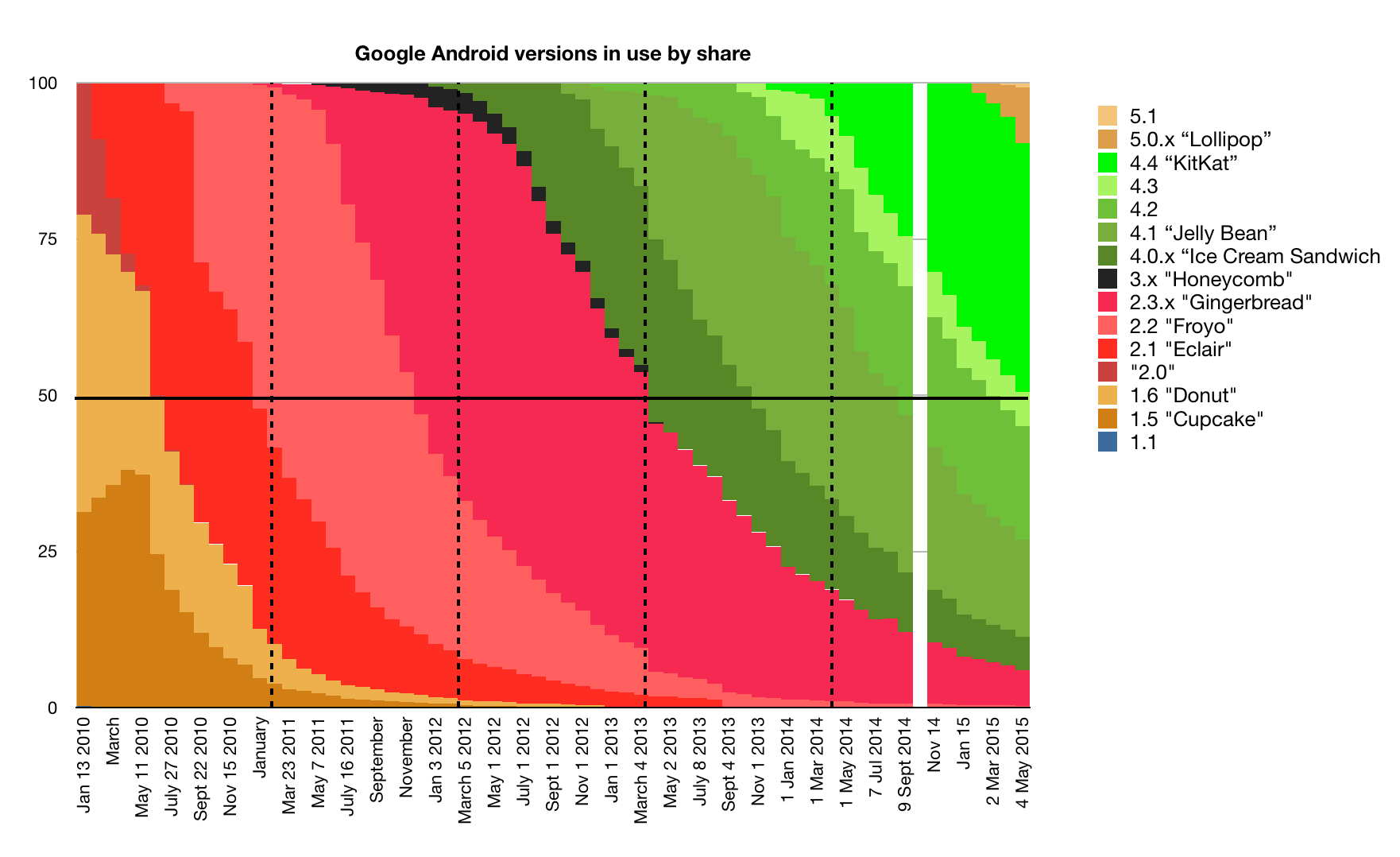

Consider: iOS 9 arrives, and lots of happy iOS users say how delighted they are to be blocking those annoying ads. (Don’t underestimate how quickly iOS 9 will be taken up: it’s going to be available for devices going back to the iPhone 4S and iPad 2 and will use less storage than iOS 8. Even iOS 8 was on half of iOS devices within two months of release.) Meanwhile Android users won’t be able to follow suit (to anything like the same extent). At least one of two things will happen:

• some Android users begin considering switching to iPhones

• Google comes under pressure to allow adblockers on the Play Store to prevent Android switching.

Neither of these is good for Google. The loss of Android users is probably more tolerable in the short term. Adblocking could pose an existential risk to Google (which is why it pays Adblock Plus’s makers to not block Google ads).

It’s unlikely that adblocking could ever reach a pitch where it really offers a grave threat to Google. But as more and more people from developing countries come online, paying for every kilobyte of data, they might want adblocking too. India in particular is a generally tech-savvy country where data prices are high; and it has embraced Android enthusiastically. Consider for a moment how that could play out.

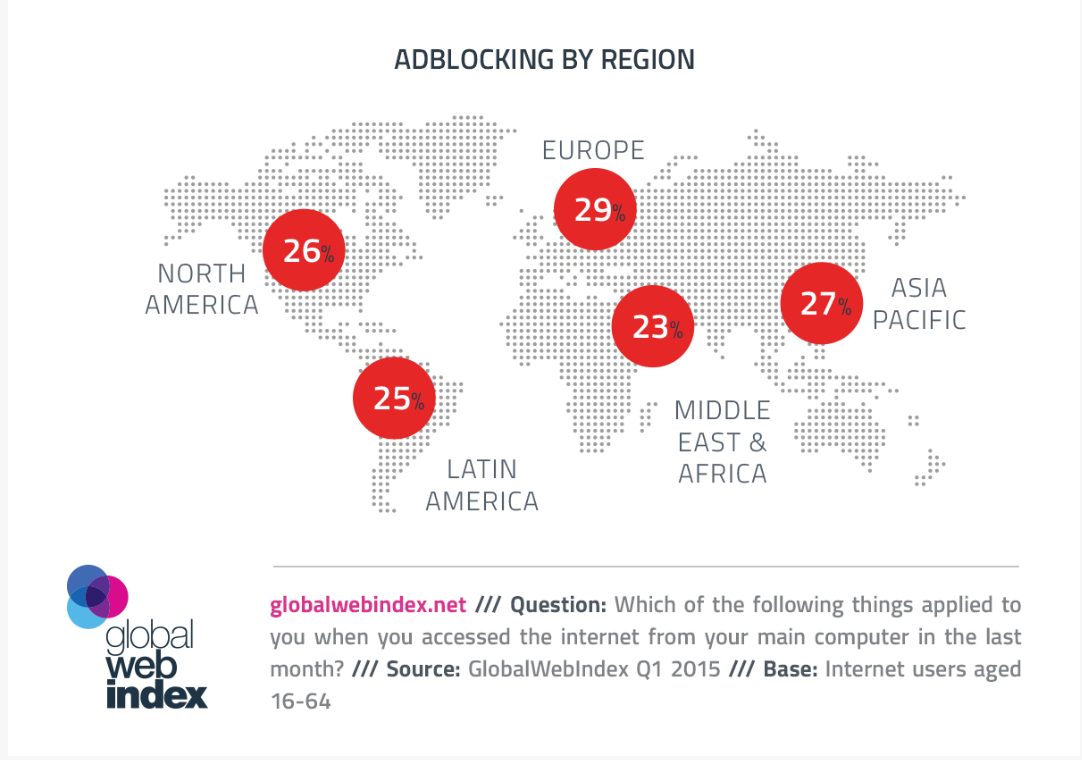

Relevantly, Global Web Index has a survey of adblocking use which found that 27% of users aged 16-64 globally in its 33-country survey had used an adblocker, and 15% had blocked tracking.

Adblocking by region. Source: GlobalWebIndex.

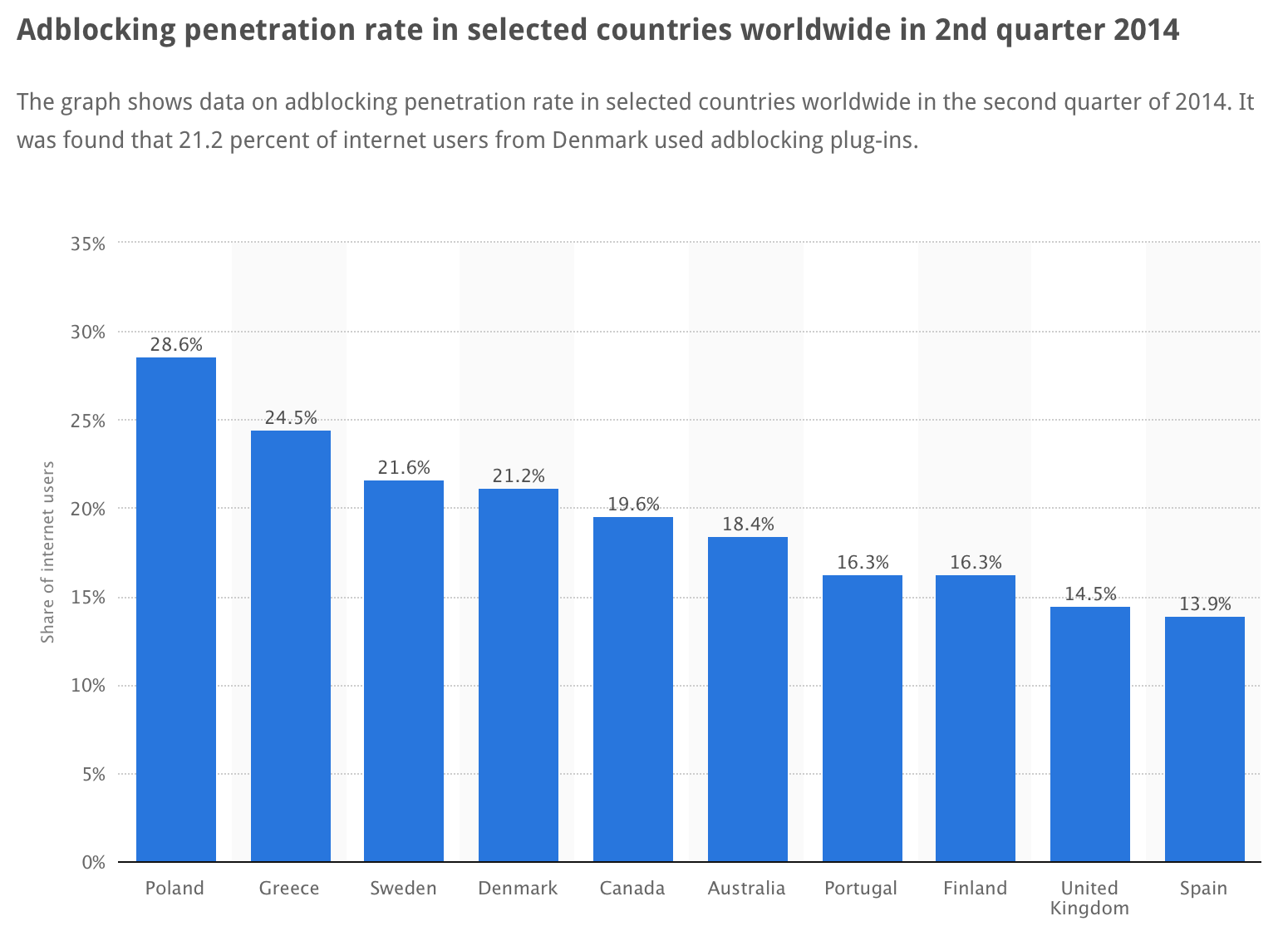

Statista also had detail about European use:

Adblocking has relatively low use – but what happens when it arrives on mobile?

Consider: hardly any of that is mobile yet. Mobile is the biggest platform. Adblocking is coming to a key mobile platform in September.

Things could get ugly quite suddenly.

Update: there’s a discussion of this post on Hacker News. You don’t need root to read it.

Like this? Other analysis I’ve done you might like:

• How Gresham’s Law explains why sites are turning off comments

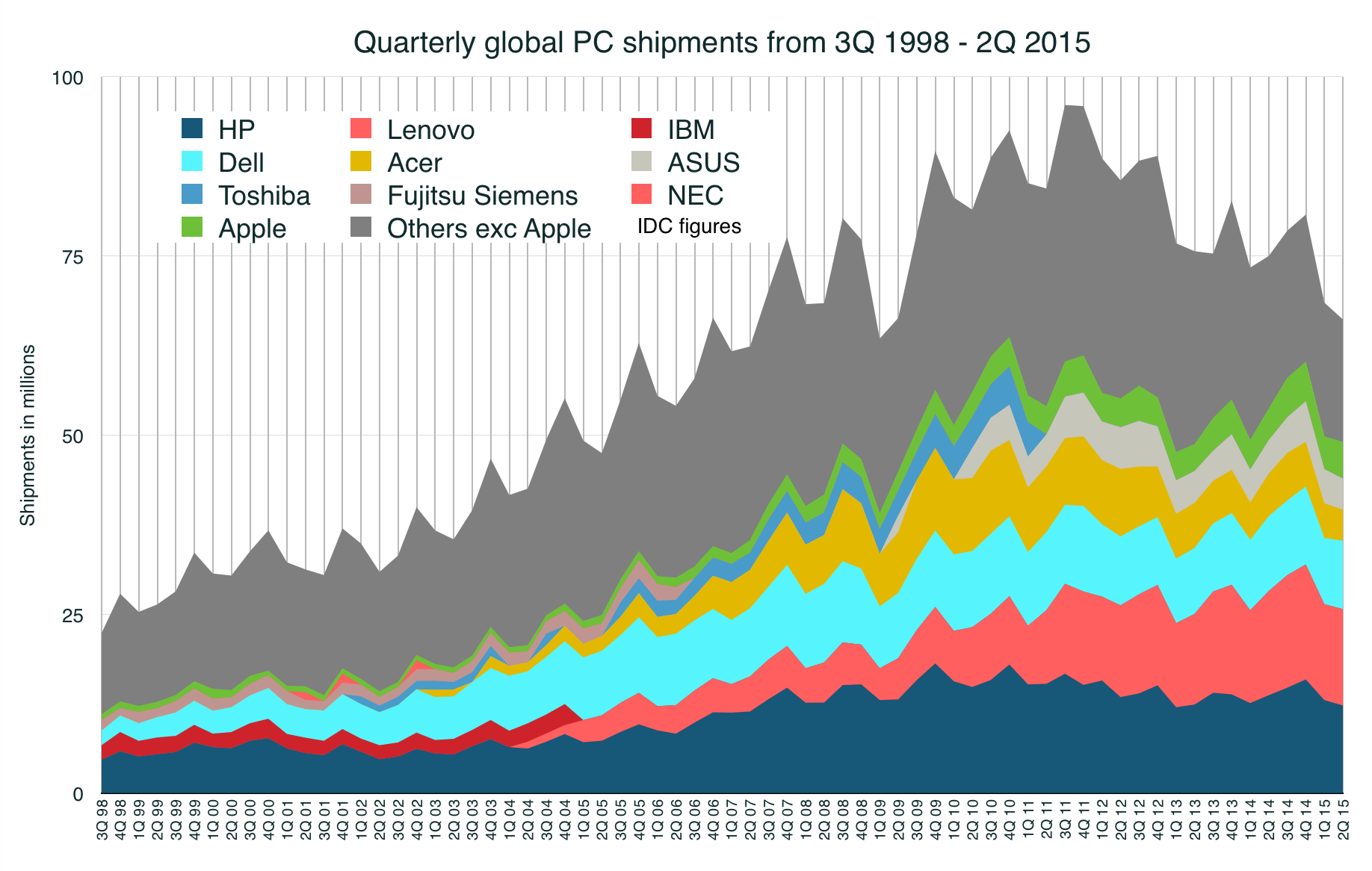

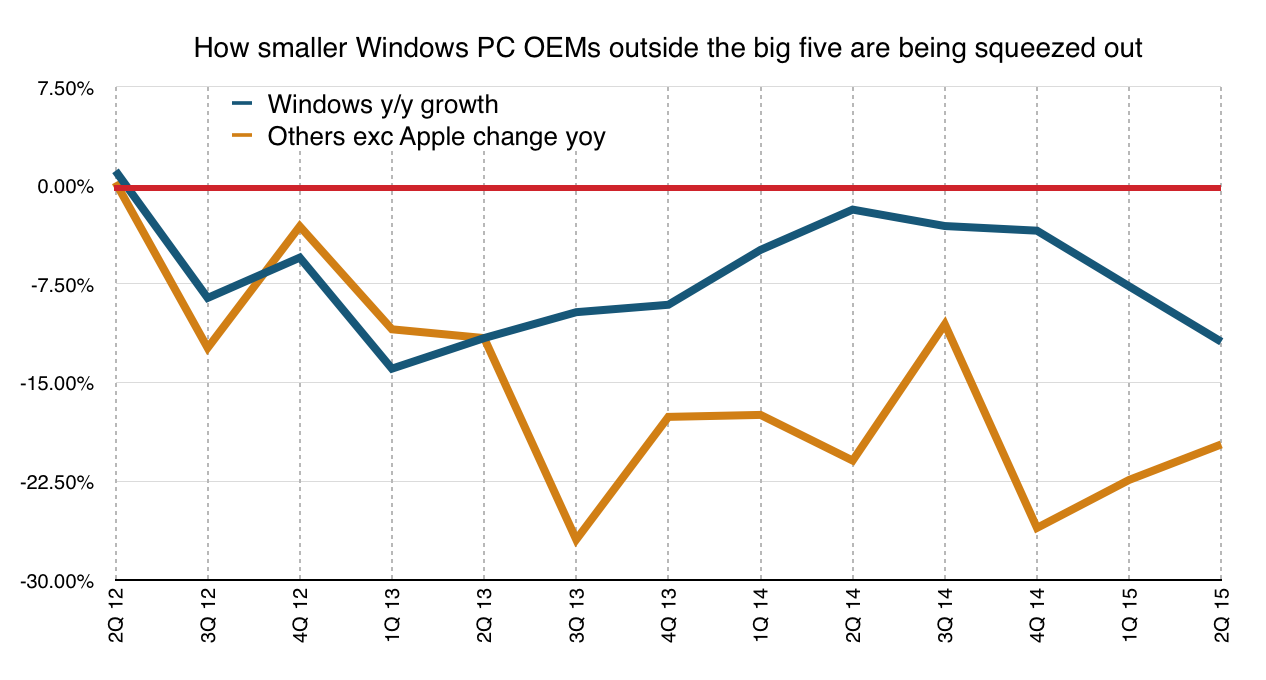

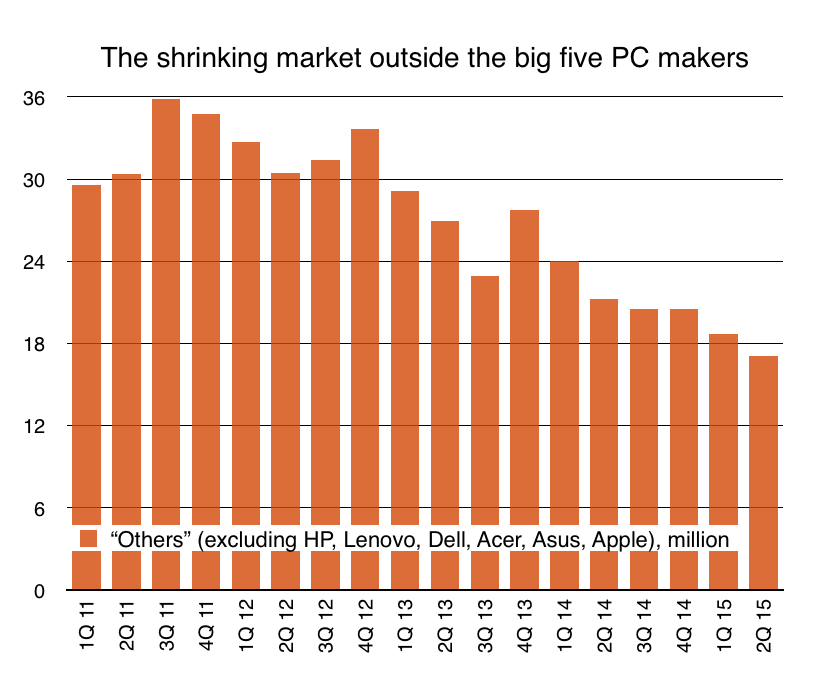

• The death of “Others”: how the PC market’s implosion is squeezing smaller players

• Android (and Apple, and BlackBerry, and Microsoft Mobile) handset profitability – the Q1 scorecard (updated)

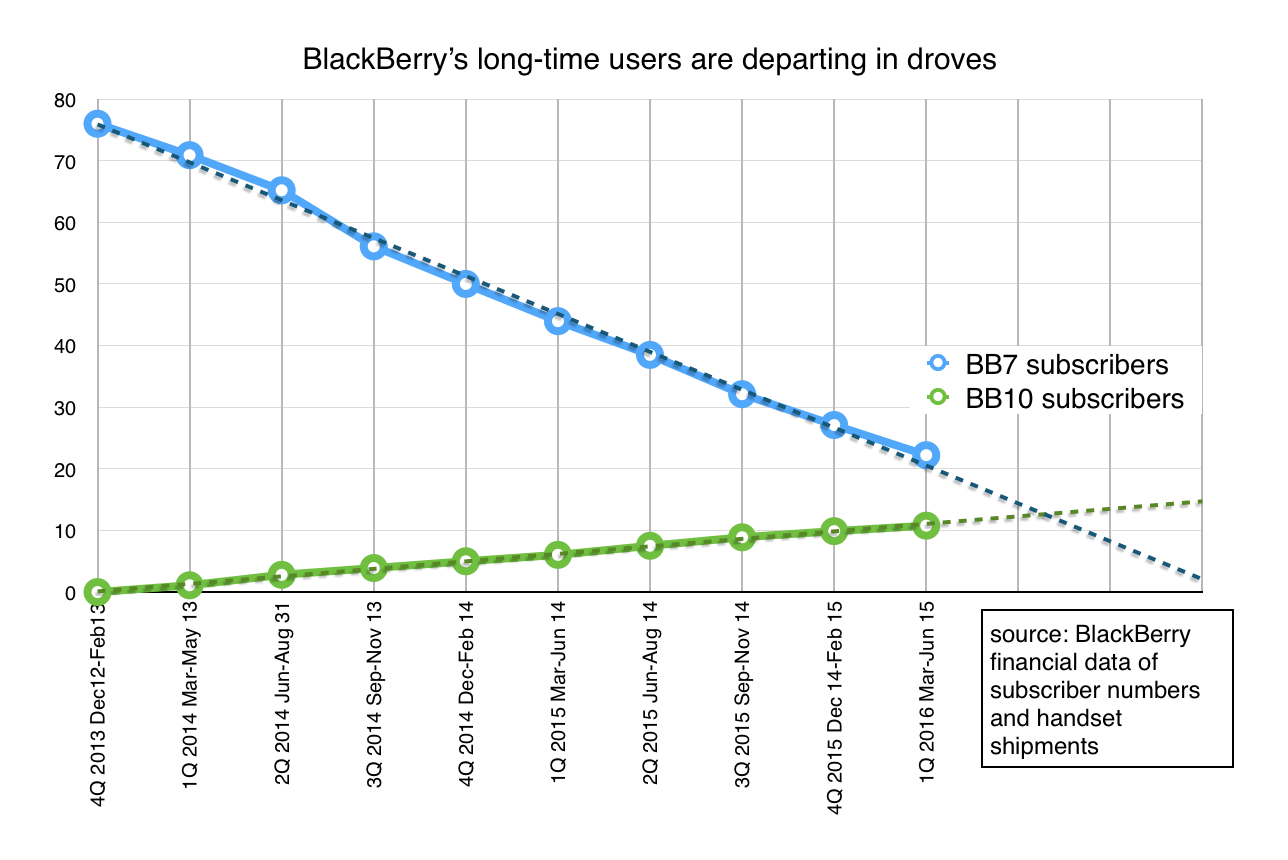

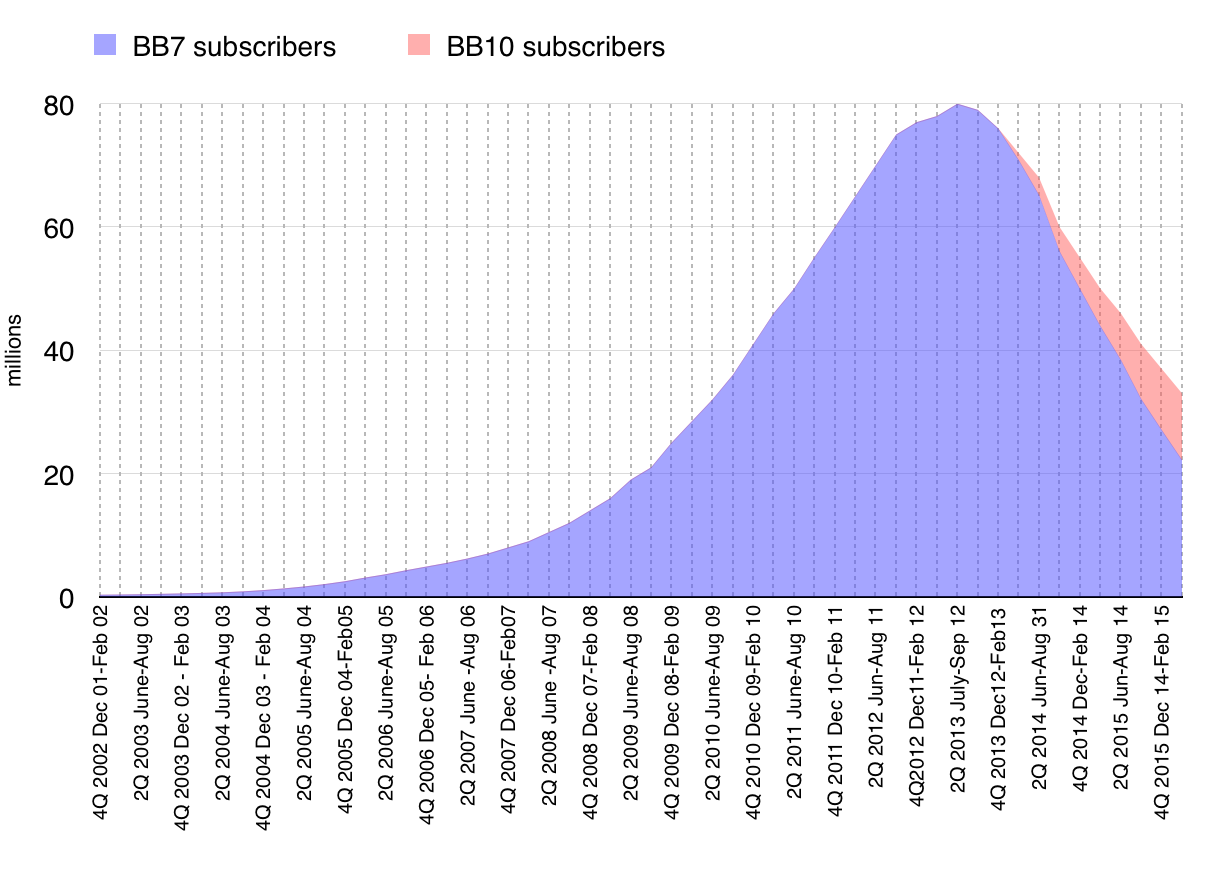

• BlackBerry might have no BB7 users left by February 2016 – and that’s a big, bad problem

Enjoy!