HTC’s stock has plummeted in the past few days after a profit warning.

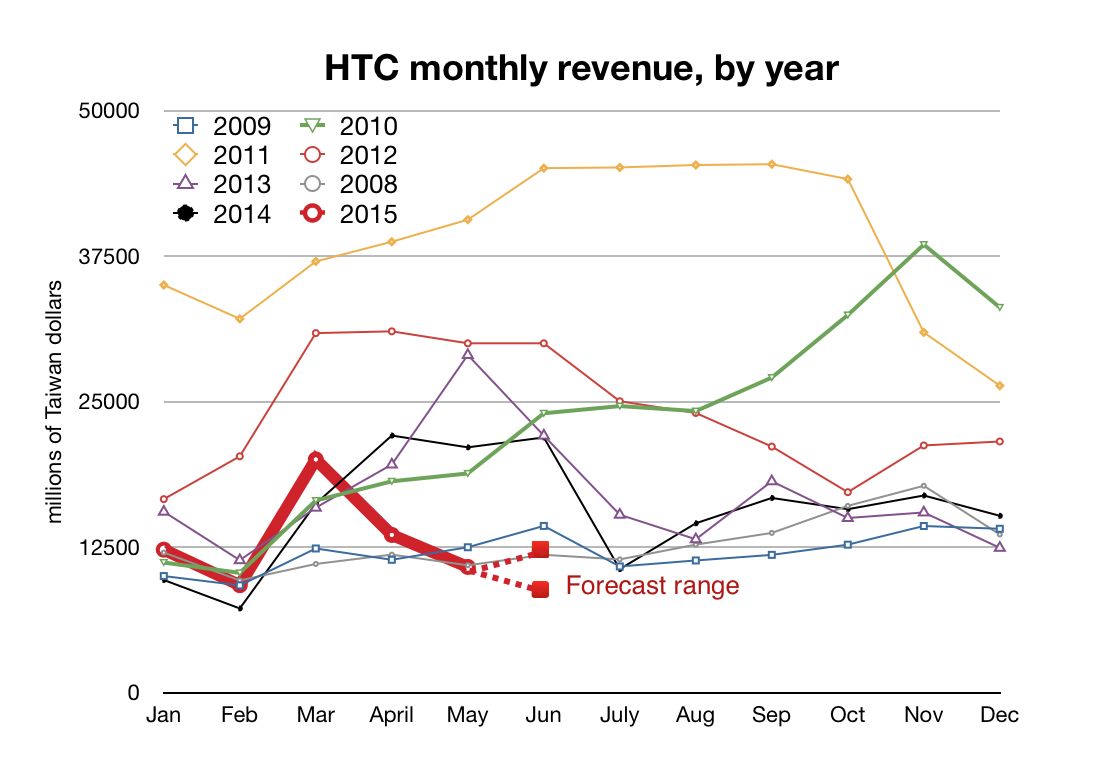

On Friday, HTC released a gold edition of its flagship M9 smartphone. Oh, hubris: the timing couldn’t have been worse. Not only did it emerge that the product promo photos had been taken with an iPhone, but within hours the company also issued a formal warning that its financial performance in the current quarter (running from April to June) would be substantially worse than it had expected. Revenues in May were terrible – down by 48% from the year before, which itself had been nothing to sing about.

Now it says that Q2 revenues won’t be the forecast TW$46-51bn (about $1.7bn), but more like TW$33-36bn (about $1.1bn) and that rather than a small profit it will make a net loss – between TW$9.70 and $9.94 per share, which is about TW$8.2bn (US$250m).

HTC has been skating along on operating margins of less than 1% for the past three quarters; cumulative net profits for that period is TW$1.47bn, or US$47m (yes, forty-seven million).

This latest news though feels like a headlong plunge into the abyss.

The forecast suggests that HTC’s June revenues will be as low as they’ve ever been since 2009 – perhaps worse.

Forecast for June is as low as 2009 – before the Android explosion.

The stock market certainly seems to think so, marking HTC’s shares down 9% for two successive days – the maximum drop allowed before “circuit-breakers” come in.

Caught in the value trap

HTC’s story is a cautionary tale about life in the value trap – when you don’t make the core software, and so have to rely on hardware differentiation and software add-ons. It has reduced the PC business to one where the five biggest Windows PC OEMs have 60% of the market, and pretty much all the profits; it’s doing much the same to the Android smartphone market, except the profits there are accruing to just one company (Samsung).

HTC’s problem is that its hardware advantage ran into the sand once Samsung really got serious about dominating the smartphone space, and now – rather like Samsung – it’s being eaten from below by Chinese rivals that do the job just as well, and at the high end is being outcompeted by LG (which has upped its game enormously in the past two years) and to a lesser extent by Sony (which offers features such as waterproofing and SD cards). Let’s also not mention those terrible adverts with the no-doubt-expensive Robert Downey Jr.

In its profit warning, HTC said:

“The change for revenue outlook is due to slower demand for high-end Android devices, and weaker than forecast sales in China, while gross margin is revised primarily on product mix change and lowered scale. At the same time, increased competition has raised operating costs for product promotion; HTC is enacting measures to further improve operating efficiency.”

In brief: the M9 (this year’s flagship) isn’t selling; Chinese buyers are buying other phones (or fewer phones altogether); it’s harder to get noticed with so many rivals; HTC’s going to cut some jobs and spending in an attempt to save itself.

HTC has been a sub-scale player for some time now – remember the calamitous delay to the HTC One in March 2013? – and to some extent the only interesting question is whether any of its attempts to escape the downward spiral can succeed. On the plus side, it’s well-capitalised, so it’s unlikely to abruptly go bust. Its key problem is how quickly it can ramp up other businesses such as its Vive VR headset and Re camera, and how much revenue they’ll generate, while it tries to rely on making smartphones that too few people want to buy.

Losing traction

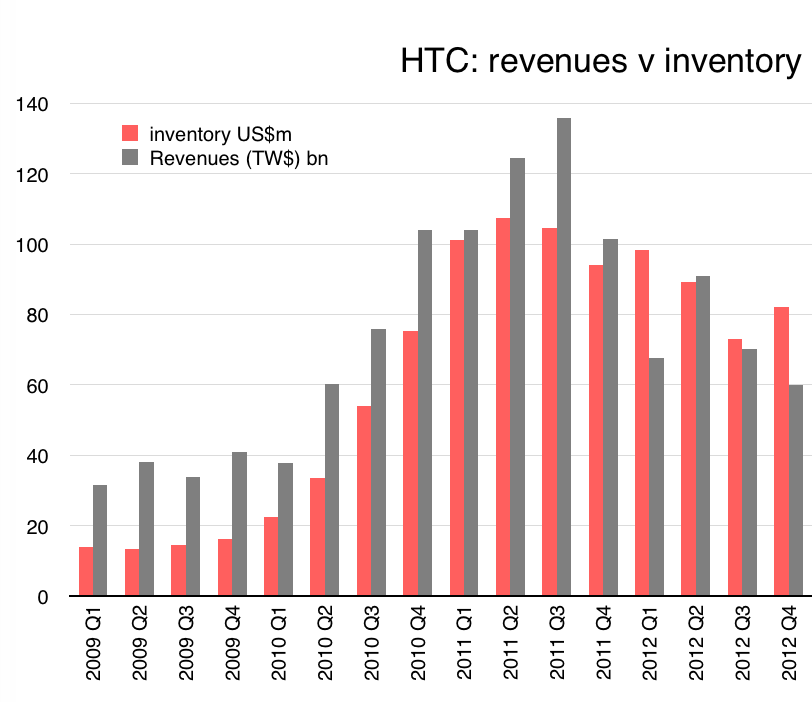

You can actually trace the point where the wheels came off by looking at HTC’s accounts, and specifically the inventory levels. “Inventory” is a mixture of goods waiting to be made into handsets in factories, work-in-progress, and finished devices.

Now compare HTC’s revenues with its inventory level. You can see that it remains largely under control through to the end of 2012 – although it’s beginning to rise as the iPhone 5 and Galaxy S3 began pushing it out of the market, meaning it was harder to sell handsets. (The lines are on slightly different scales: by the end of 2012, inventory was about 40% of revenue.)

Revenues kept ahead of inventories, at least to the end of 2012…

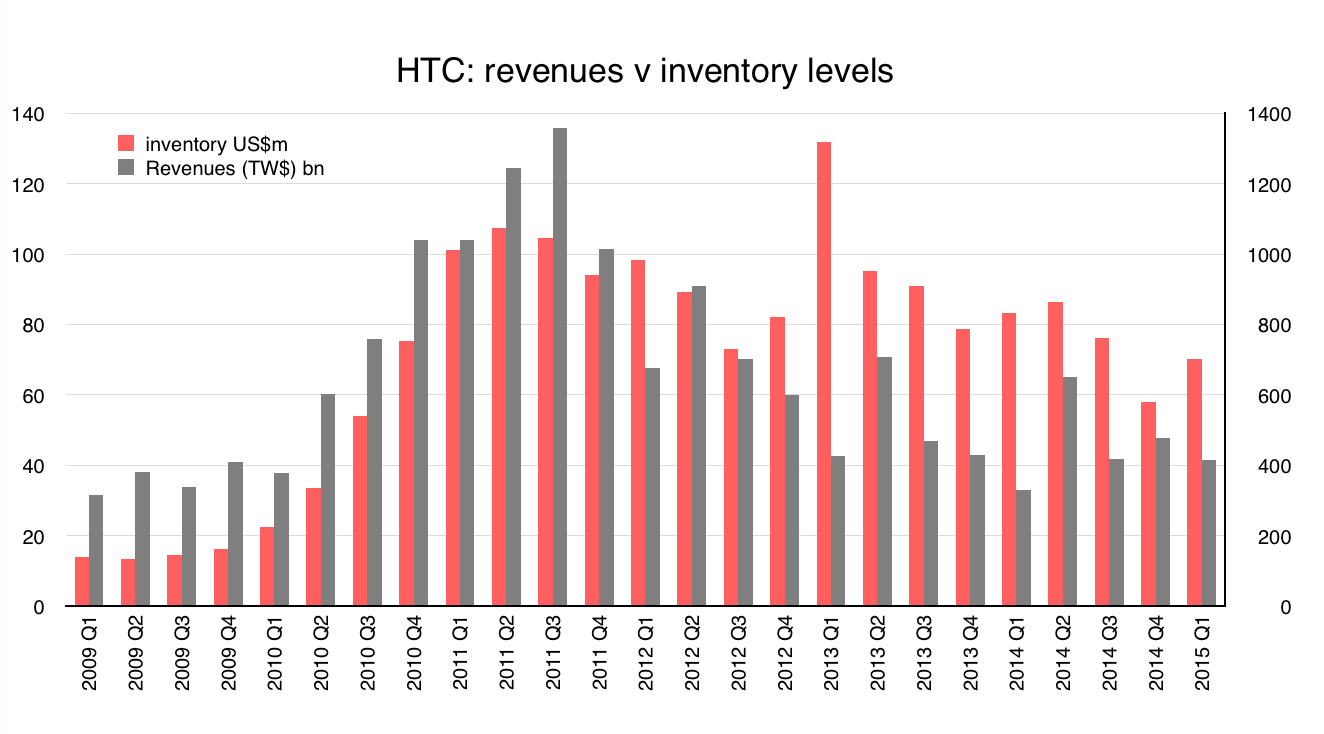

But in 2013, it hit that problem sourcing camera sensors for the HTC One M8 (the original – thanks Matjaz Ropret). And it shows up in inventory: all those goods sitting in factories and warehouses waiting to be shipped. Inventory spiked to 89% of revenue for the quarter. Revenues have tracked down, and inventories have stayed relatively high (above 35% of revenue, and sometimes 76%) ever since. High inventories are bad because they’re goods that you’ve paid for, but can’t sell; they’re a drag on business, and what’s worse is that as they age they drop in value. Tim Cook described inventory as “like milk – it goes off after a few days”. (Apple’s inventory is consistently below five days of hardware sales.) HTC had 45 days’ worth of inventory at the end of Q1; watch out for the figure at the end of June, because it will tell us how the M9 has sold to carriers, if not end users.

Suddenly at the end of 2012, things go out of control…

Basically, the inventory story breaks into two parts – green marks the OK stage, and red the point where it’s gone bad:

The red period, from the end of 2012 on, shows inventories growing way above associated revenues

(This, by the way, is why it matters to look at company accounts. You can find stories if you read them closely enough. That’s where I found BlackBerry’s PlayBooks piling up in 2011.)

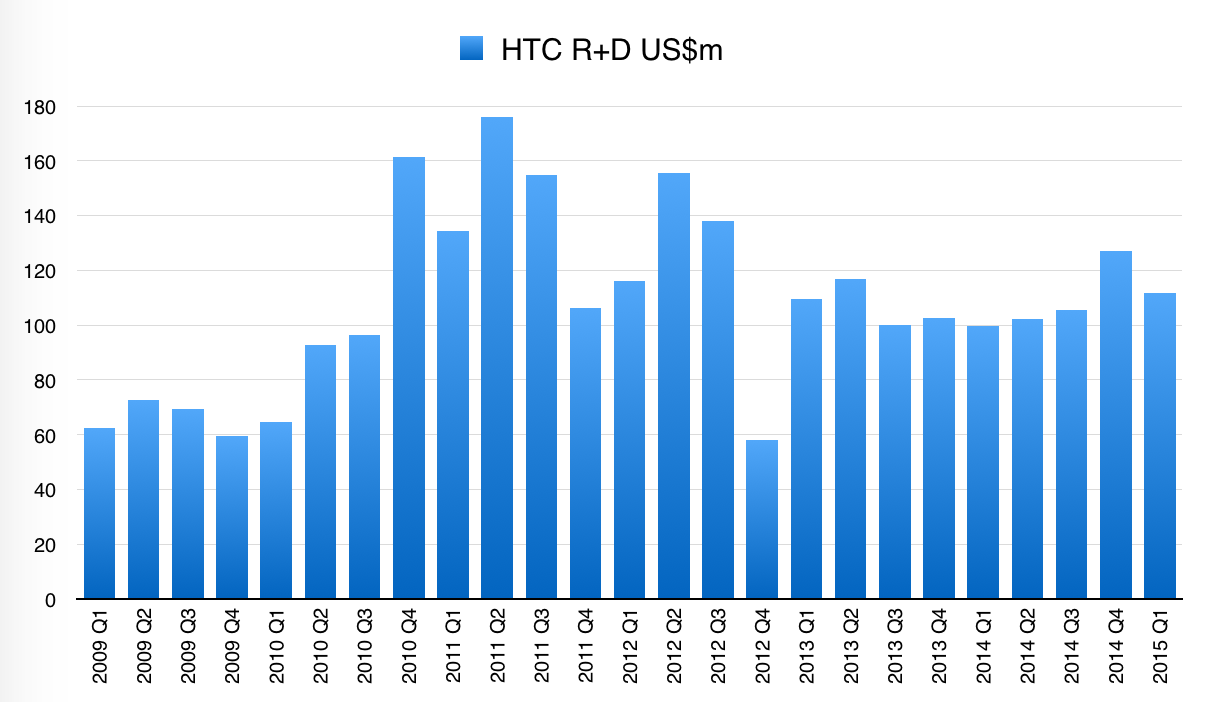

The company’s caught in a bind. It doesn’t make enough profit to invest in really top-level R+D that might let it break through into new spaces. Here’s its R+D spending by quarter, in US dollars:

With spending at about $100m per quarter, HTC can’t break out of its position as a mid-tier smartphone maker.

It’s pretty hard to spot where it is spending money on the HTC Re camera, or the HTC Vive VR headset. The latter seems like a smart move (whereas the camera is a complete commodity product whose minimal margins will get eaten by rivals, just like in the phone market). HTC’s in there comparatively early, and has a deal with Valve. I wouldn’t rely on that being the saviour of the business, though.

In search of a USP

So how does HTC get out of this? A better way to ask the question is: what’s HTC’s unique selling point (USP)? What does it bring to the smartphone and device party that nobody else does? Apple has its brand and vertical integration; Samsung has scale and vertical integration (it makes the chips and displays for its own phones); LG has vertical integration; Sony has its brand and terrific photo sensors, though I don’t think that’s necessarily sufficient for the survival of its smartphone business, it is at least a USP.

HTC doesn’t have a geographical advantage (it’s not in China, it’s in Taiwan); it doesn’t have a vertical integration advantage. It isn’t developing the software, though its Sense overlay for Android is nice. There’s no point making Windows Phone handsets, because they don’t sell except at the low end, and there’s no profit there.

Contrast BlackBerry and HTC: both are now pulling in roughly the same revenue per quarter (sub-$2bn). BlackBerry sells far fewer handsets than HTC – only 1.6m in the December-February quarter, and by my estimates perhaps 1.3m in the March-May period, while HTC shipped around 5m handsets in Q1.

BlackBerry’s advantage, though, is that it has a cushion of customers, particularly in enterprise, who are willing to pay subscription fees. If handsets were all BlackBerry had, it would have gone bust long ago.

HTC doesn’t have that cushion. So what does the future look like? At one time in 2012/3, Amazon was interested in buying it – but Cher Wang, its chair (and now CEO, having pushed Peter Chou over to the “future products” side) turned Jeff Bezos down. That looks like a bad decision. Short of a miracle, it doesn’t look like anything’s going to pull HTC out of the mire.

Pingback: Qué debe hacer HTC para volver a ser un fabricante fuerte - LIDDIT

Pingback: Qué debe hacer HTC para volver a ser un fabricante fuerte - ANDROID DOMINICANO - Blog sobre el sistema operativo móvil de Google

Pingback: Start up: Grexit to bitcoin?, Google’s antitrust deadline, Merkel’s suspect PC, Samsung security hole and more | The Overspill: when there's more that I want to say