How much did this Lumia 920 cost to make? And will it have a successor? Photo by Whatleydude on Flickr.

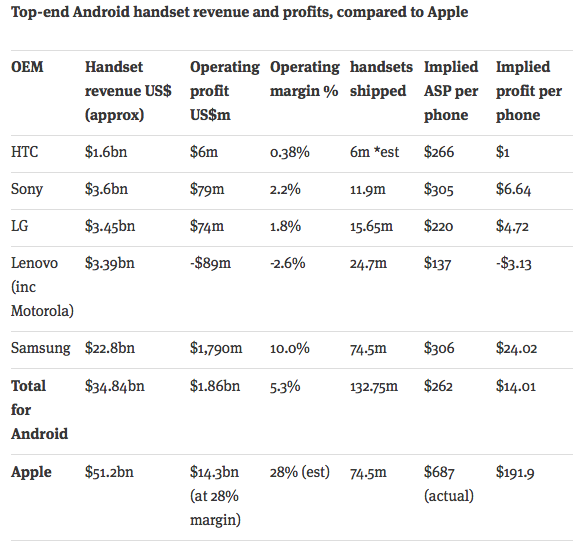

In case anyone was in any doubt, Microsoft’s results last week demonstrated once more what we’re coming to know about the mobile handset industry: it’s damned hard to make any money in it. When I published a fairly simple analysis of the state of the top-end Android handset market (with a comparator to Apple’s iPhone profits), people were apparently flabbergasted by how thin the per-handset operating margins were on these devices which sold for hundreds of dollars.

See the original post for more detail and caveats.

But Microsoft showed that it’s not even able to generate gross margin while selling millions of handsets. (Gross margin is the difference between how much it costs you to make the item – usually factory costs and distribution costs – and what you get for it. Gross margin normally excludes R&D and sales & marketing costs; to get the operating profit, you subtract those costs too, so operating profit is always less than gross margin.) My analysis of Android handset makers looked at operating profit.

Negative gross margin takes some doing; spending more making stuff than you take in for it is exceptionally bad business. But Microsoft Mobile did, officially: take a look at Microsoft’s 10Q for the calendar first quarter of 2015.

It says

Phone Hardware revenue was $1.4bn in the third quarter of fiscal year 2015, as we sold 8.6m Lumia phones and 24.7m non-Lumia phones. We acquired NDS in the fourth quarter of fiscal year 2014. Phone Hardware gross margin was $(4) million in the third quarter of fiscal year 2015. Phone Hardware cost of revenue, including $147m amortization of acquired intangible assets, was $1.4bn.

For those unversed in accountancy notation, that “$(4) million” means “minus $4 million”. Accountants use brackets rather than a minus sign because it’s easy to overlook a minus sign and create a horrendous hash in your calculations.

For the nine months,

Phone Hardware revenue was $6.3bn in fiscal year 2015, as we sold 28.5m Lumia phones and 107.3m non-Lumia phones. Phone Hardware gross margin was $805m in fiscal year 2015. Phone Hardware cost of revenue, including $401m amortization of acquired intangible assets, was $5.5bn.

This does take some untangling. In my analysis, I’m going to ignore the writeoffs (amortisation) of intangible assets – essentially, goodwill (“how much more we paid than the physical assets are worth”) being written down. This actually makes the gross margin look better – as in, in positive territory. That’s a start.

Pause for history

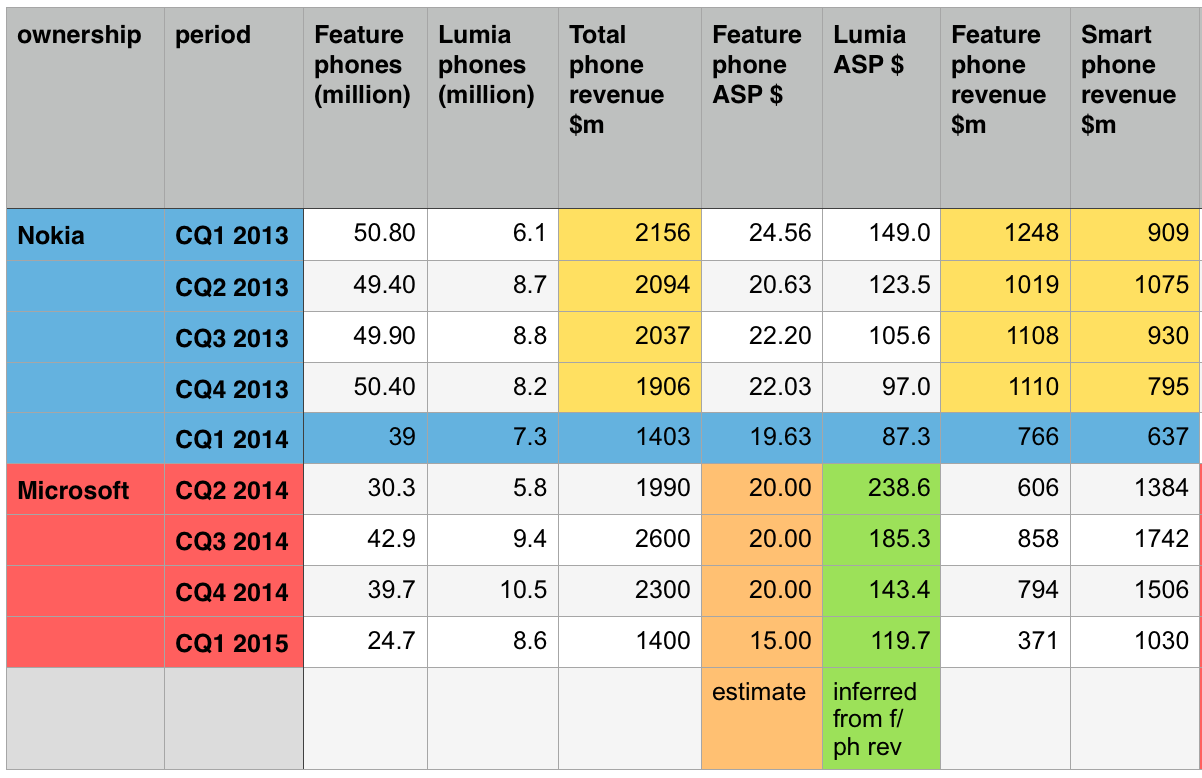

Some brief history. When Nokia made phones, it used to provide wonderfully detailed results, in which it would tell you how many featurephones and smartphones it had sold, and at what average selling price (ASP). This made it easy to see how its business was going. It didn’t give you gross margins – only operating margin for the whole phone business. In general, though, we knew its featurephone business was profitable, and that once it moved to the Windows Phone Lumia range, the smartphone side lost a ton of money.

Enter Microsoft, buying Nokia’s phone business – including featurephones – for €5.4bn, which was completed on April 25th 2014. That’s when the featurephone and Lumia sales start showing up in Microsoft’s results, and we shift to the “gross margin” measurement. (Microsoft does this because Steve Ballmer reorganised it to an Apple-style “apportion all cost across the board”, rather than making each division its own profit-and-loss fiefdom.)

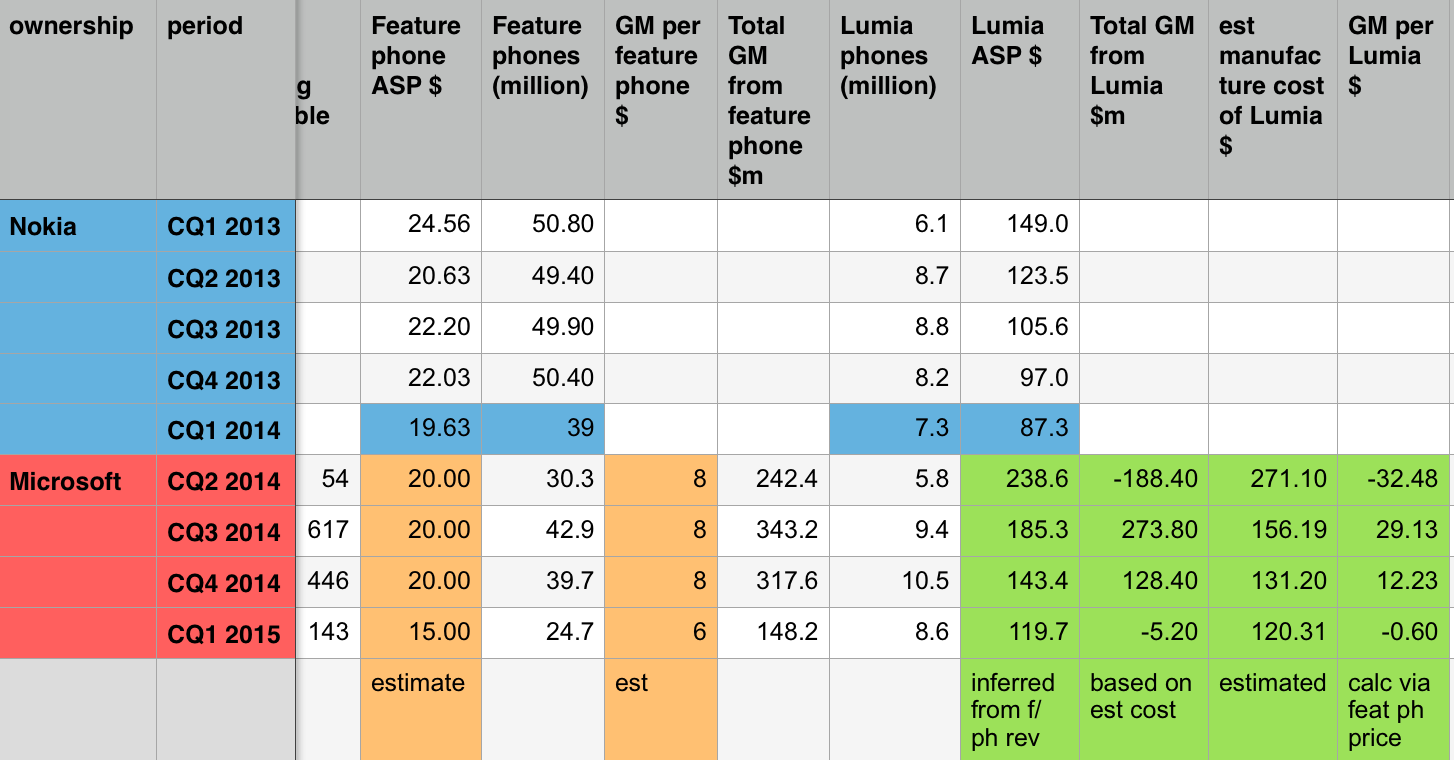

Given the Lumia ASP and sales figures at Nokia, you could work out the ASP of featurephones, and their contribution to revenues. What I’ve done in the table below is use Nokia’s featurephone and Lumia ASP (converted from euros to dollars at the prevailing rate at the end of each quarter) and try to carry that forward to estimate the recent ASPs of Lumia handsets under Microsoft’s ownership, and their contribution to revenues.

If you estimate the ASP for featurephones based on the Nokia numbers, you can figure out those for the Lumia phones at Microsoft.

A few things to note: I’m assuming that featurephone ASPs are falling. Even with that, there’s a clear fall in the ASP of the Lumia phones – from (a really quite high) $238 in the second calendar quarter of 2014 to the present. There hasn’t been a flagship phone released in that time, so perhaps not surprising.

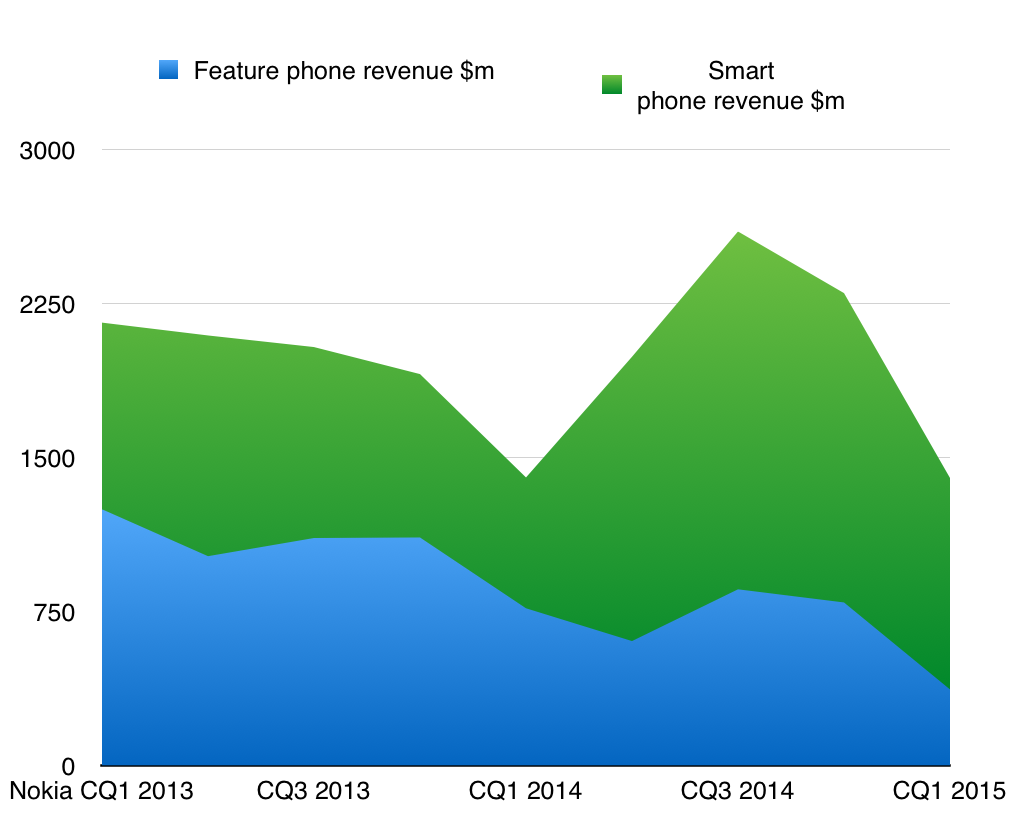

Also, smartphone revenue has flipped from being the minority source at Nokia to being the majority source now (even at $20 featurephone ASP, it’s still like that) because featurephone sales are collapsing, while those of smartphones are remaining fairly static – like this:

Based on ASP assumptions, you can figure out how much revenue smartphones and featurephones generate. That’s not profit, though.

Now we move on, to seek out gross margin. There’s no data from Microsoft about the separate gross margins of the featurephones or Lumias. We don’t know how much they cost to build, or which might be profitable. So we have to use estimates and what people tell us.

Fortunately, we do have some indication of how profitable Nokia featurephones were. In an interview in April 2013, Nokia’s director of platform and content said that the profit margins on the $20 Nokia 105 were the same as those on the Lumia phones. How much might that be? Again, we don’t know, but it can’t be a lot. Putting it at $5 seems reasonable.

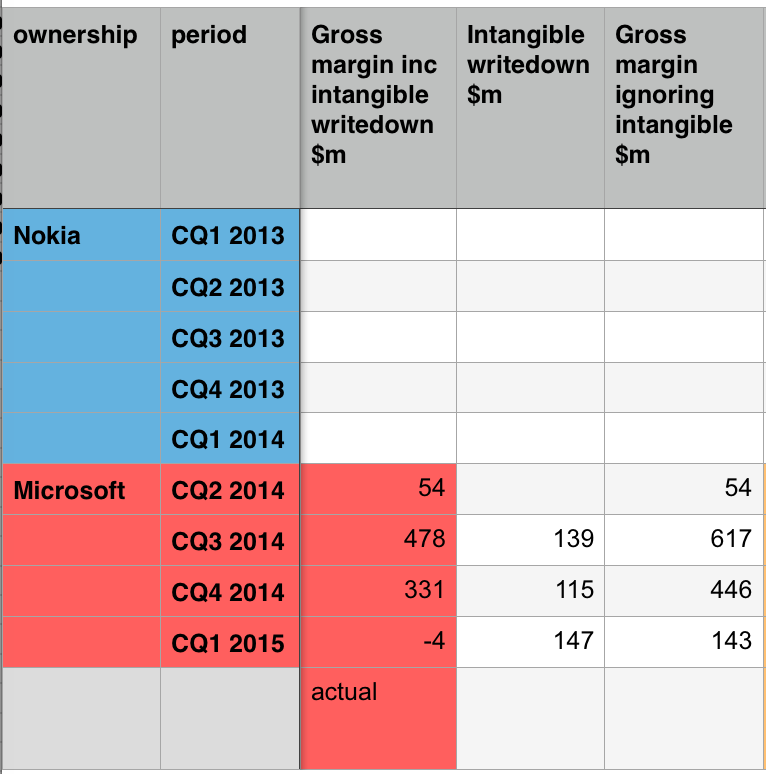

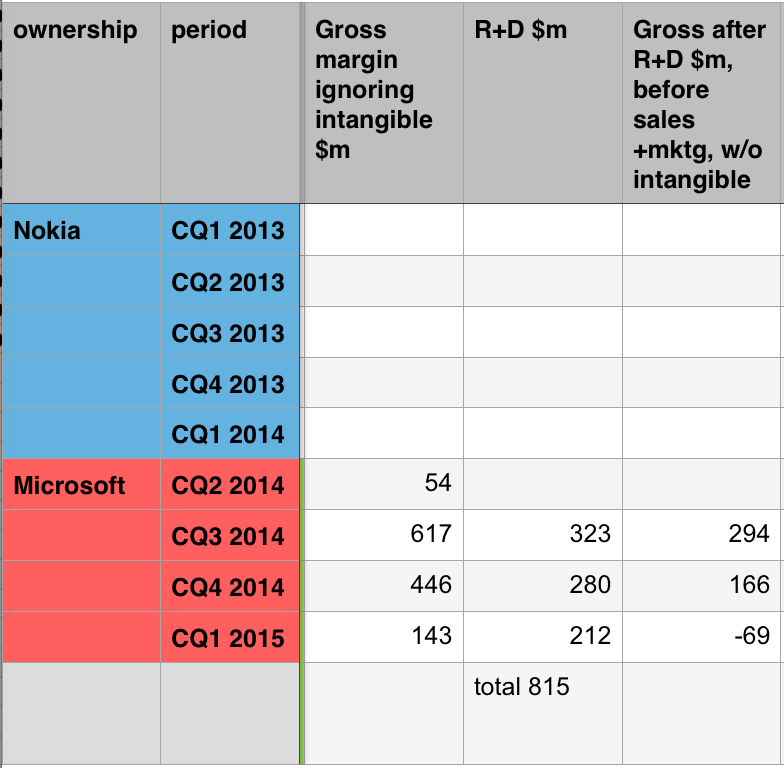

We have the figures for total gross margin; we also have the intangibles writeoff in the financials. So that gives us a “real” gross margin (ie the day-to-day gross margin for the quarter, excluding accountancy writeoffs):

Microsoft gives quarterly figures for intangible writeoffs; subtracting that gives the hardware gross margin.

Now we make assumptions about featurephone gross margin. I’ve gone for $5, falling to $4 as the average price of the handset falls from $20 to $15.

From this, and from the data we’ve got about total phone shipments, it’s quite simple to back-calculate to come out with figures for the total contribution to gross margin by featurephones and Lumias.

If we assume per-handset profit on featurephones, we can use that with the GM data to figure out how much Lumias cost to make. And we have the ASP..

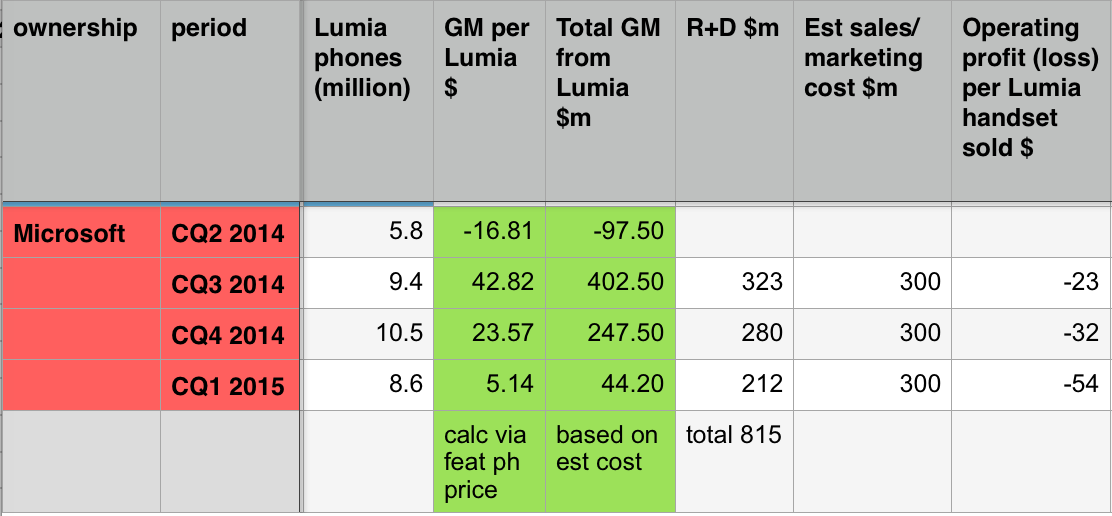

Which tells us what? The CQ2 figure is anomalous – Microsoft mentions an intangibles writeoff in that period, but doesn’t specify how much (unlike other periods). It’s likely the total gross margin was larger if you ignore that, which would put the gross margin per Lumia into the black.

What we also see is that even if we allow a miniscule per-handset gross margin for each featurephone, we see a rapidly falling gross margin for the Lumia line. Here’s an alternative scenario, if we think that the featurephones have a $8 gross margin, falling to $6 in the latest quarter:

Giving a per-handset profit of $8 for featurephones makes the Lumia business look much worse. It’s unlikely, though.

On this higher profit for featurephones, the Lumia gross margin goes into negative territory. You can argue that’s too high a margin for a featurephone. Doesn’t matter though – the direction of travel is clear: the Lumia barely washes its face.

And this, don’t forget, is before you include the costs of sales and marketing – all those Lumia ads! – and research and development. Here’s the R+D impact:

Three months ended March 31, 2015 compared with three months ended March 31, 2014: Research and development expenses increased $241 million or 9%, mainly due to increased investment in new products and services, including NDS expenses of $212 million.

For the nine months:

Research and development expenses increased $694 million or 8%, mainly due to increased investment in new products and services, including NDS expenses of $815 million. These increases were partially offset by a decline in research and development expenses in our Operating Systems engineering group, primarily driven by reduced headcount-related expenses.

A little digging shows the R+D costs for the NDS (Nokia Devices and Services) segment by quarter. That gives us a sort of “halfway” operating profit once you deduct R+D, which shows that the division has moved into the red even before you consider sales and marketing costs.

R+D numbers are mentioned in the quarterly 10Q. To get towards the operating profit (or loss), we need to subtract that.

That’s not profit

To figure out whether the handset division makes an operating profit we’d have to know the sales and marketing costs. It’s pretty improbable that those were anything less than $300m per quarter (that’s $10m per day, worldwide). Which means that Microsoft’s handset division has been loss-making since it took it over, despite those profitable featurephones, and ignoring the writedown of intangibles.

On a per-handset basis, if you allow $300m per quarter for sales and marketing (into which we’ll also roll administration), then you get a clear picture: Lumia handsets don’t make an operating profit at all.

Don’t forget, this relies on assumptions around featurephone profitability and price.

But hey, you say, that’s all assuming that featurephones are making $5 per handset. What if it’s $0? No problem – that’s the fun of spreadsheets. You can play with assumptions:

Lumias still show a per-handset loss. (Remember this is with featurephone pricing of $15 in the latest quarter.)

OK, dammit – what if featurephones lose $5 per handset? Lumias still plunge into operating loss in the latest quarter – and remember, this is ignoring intangible writeoffs, and allowing just $10m per day worldwide for sales and marketing:

Even at a $5 loss per featurephone, Lumias aren’t moneymakers at the operating level (on my assumptions).

You might have thought that Android handset makers had it tough, but at least – at the top end – they’re ekeing out something.

(Yes, these numbers are based on assumptions about featurephone pricing and margin, but I’d defend them as all being reasonable based on what we know about the business in the present and past.)

Update: thanks to Vlad Dudau of Neowin, who pointed me to Microsoft’s discussion of its results, where they say

We have made significant progress in reducing the operating expense base in the Phone business, moving from an annualized rate of $4.5bn at acquisition to a run rate under $2.5bn.

Opex is R+D plus sales+marketing and things like general+administration; an annualised run rate of $2.5bn is $625m per quarter – which is slightly more than I was allowing there. That would make the Lumia margins worse.

Microsoft adds:

That said, the changing mix of our portfolio to the value segment and the significant negative headwind from FX [foreign exchange rates] will impact our ability to reach operational break even in FY16.

So, no good news in the offing. (/Update.)

Why carry on, then?

Why, then, does Microsoft persist with Windows Phone? It can’t really think that it’s somehow going to come good and suddenly take off to challenge iOS and Android. The idea (which some outside Microsoft cling to) that the introduction of Windows 10, where apps can be written for both desktop and mobile, will suddenly lead to a huge uptake (by businesses?) is pie in the sky. Mobile and desktop have different design demands. Corporations with mobile needs haven’t been sitting on their hands for the past five years waiting for Windows Phone to reach a sort of maturity; they’ve been hiring people who can hook into their systems using iPhones and Android phones. Under Satya Nadella, Microsoft has recognised this, offering Office and other key software on rival platforms to capture (or retain) users and revenue.

You can’t justify it on “they’ll make it back in profits on services”; the 80m or so Lumia owners around the world aren’t the high-end users, but low-end ones who are less likely to spend on apps, or pricey Microsoft products.

So why? Two clear reasons. First, it’s important to keep playing in this space; Microsoft needs to have a mobile offering because it’s impossible to say where in the future a mobile-focussed offering might be key.

Secondly, though, is that more simple one: pride. Couple that with the inertia of a big organisation, and the fact that in the scheme of Microsoft’s profits the losses from the mobile division (about $500m, ignoring intangibles, over the past three quarters) are piffling, and there’s no reason to stop.

However, things could change. I’ve argued previously that Nadella should just give up on Windows Phone, and move to an Android fork. Not long after I argued that, Nokia (then still Finnish-owned) introduced the Nokia X, using Microsoft services and AOSP (Android without Google services on top). Microsoft rapidly killed it.

But now Microsoft is preinstalling its apps on the Samsung Galaxy S6 – and more importantly, has a “strategic partnership” with Cyanogen. The latter is a huge, and smart, move: it seems to me the easiest way for Microsoft to make a real impact on mobile.

If the Cyanogen move takes off, though, I could see Windows Phone withering. Why bother with loss-making hardware when you can piggyback on the world’s most successful mobile OS (that’s Android/AOSP) for the pure gravy of services profit? I wouldn’t.

Other posts you might find interesting:

• Android OEM profitability, and the most surprising number from Q4 2014

• Why Google’s struggles with the EC – and FTC – matter

• How Gresham’s Law explains why news sites are turning off online comments

Piggy-backing on your first reason: I wonder if Microsoft feels a need to maintain a toehold in the mobile market so that it’s ready to make quick moves into _non-phone_ hardware. HoloLens looms large; any expertise gleaned from building Lumia phones seems likely to improve that product. The Microsoft Band, likewise.

Good analysis, but there is no good reason for Microsoft to continue to dig deeper into a hole. Get out of the hardware business and get out now.

Over all I agree. However enabling Android apps on WP rather than making an Android phone seems more likely. An Android fork has implication beyond the mobile sphere. Also internally resources they have like engineers and knowledgebase just does not align with supporting a new OS and new ecosystem.

A better question is can Windows go beyond mobile into things like Hololens and IoT and 80 inch screen. If yes then MS might be ok having a tiny share in mobile as long as the Windows ecosystem grows.

Also on the other hand they want to sell computing. They want people to use Azure even if one wants to use PHP or node or any other tech.

I didn’t mean “making an Android phone”. I meant piggybacking on whatever Cyanogen does, which might be to team up with a handset maker.

Pingback: Oh, and also: Microsoft’s warning it might write down the mobile division | The Overspill: when there's more that I want to say

Pingback: Android (and Apple, and BlackBerry, and Microsoft Mobile) handset profitability – the Q1 scorecard | The Overspill: when there's more that I want to say

Pingback: Windows Phone: Microsoft’s really good reason to keep it going isn’t about phones | The Overspill: when there's more that I want to say