Google UK: it’s either gigantically expensive to run, or there are tax shenanigans going on. Photo by osde8info on Flickr.

The UK is the only region besides the US for which Google breaks out revenue in its quarterly earnings, because – for whatever reason – the UK represents 10% or more of Google’s total revenue. (Public companies are generally obliged to cite countries or regions which generate more than 10% of revenue in their results.)

Google doesn’t, however, break out profits for any region; it just gives a single figure for operating and net profit.

Update: note that this post doesn’t take into account any of the amazing workarounds that companies use to shift “activity” from one place to another; for example, Google doesn’t even accept that it has a “place of activity” in the UK. For instance, look at Jolyon Maugham’s analysis, and especially the comments that follow it.

But what if we were to try to estimate (in a fag-packet way) how much profit Google has made in the UK, and then compare that to the tax it has paid, and the tax that it recently paid in a settlement with the UK’s tax authorities, HM Revenue & Customs?

Tax, of course, is payable on profit, not revenue. And it’s helpful too to compare Google with other UK media companies which sell advertising and have other activities.

So take a look at the tax paid by another UK-based media company of comparable size – ITV.

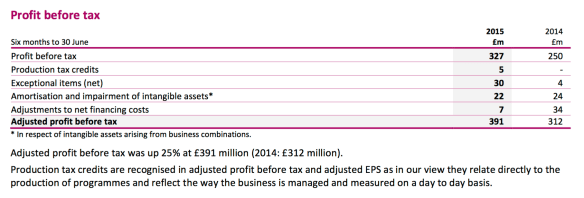

ITV’s interim results (for the six months to end June 2015) show six-month revenues of £1.53bn, with profit before tax of £391m, compared to profits for the same period in 2014 of £312m. And here’s the profit before tax figures (for six months).

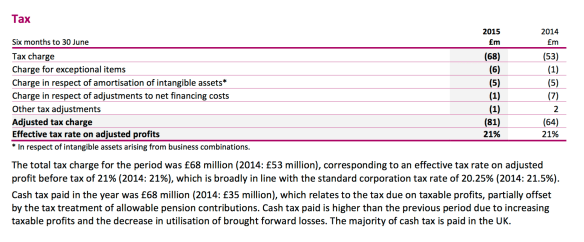

On which it paid tax of £81m (first six months of 2015) and £64m (first six months of 2014) – an effective tax rate, as it points out, of 21%.

On which it paid tax of £81m (first six months of 2015) and £64m (first six months of 2014) – an effective tax rate, as it points out, of 21%.

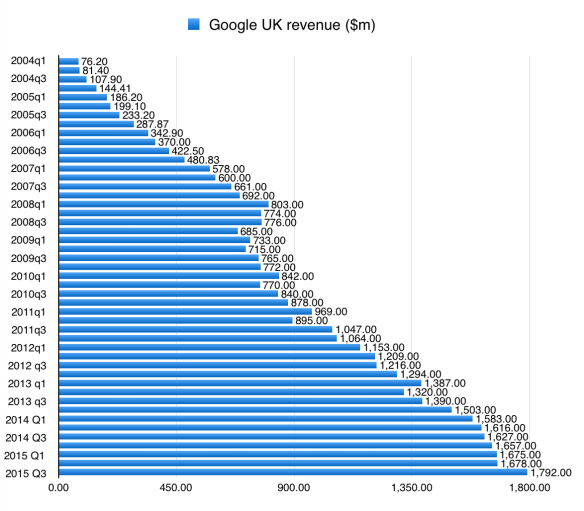

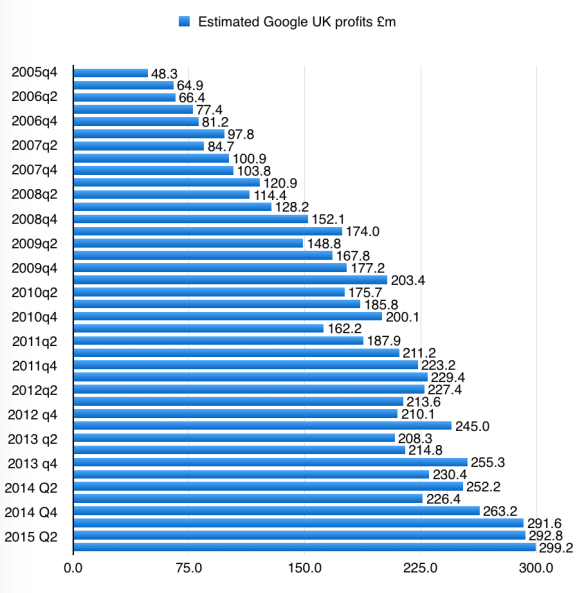

Now let’s move on to Google. Its UK revenues are as follows – all given in US$:

Note that these are a LOT more than ITV’s. But how do we get from this to its profits? The simple way is just to adopt the overall profitability of Google, the corporation. As a rough-and-ready way of approaching Google’s UK profits, it will have to suffice. The UK doesn’t have the expense of the “moonshot” operations such as self-driving cars; most of the activity is around advertising, though there is also an Android development team (whose work is allegedly actually “happening” in California for tax purposes) and various building works which will all affect immediate profitability because they’re expensive.

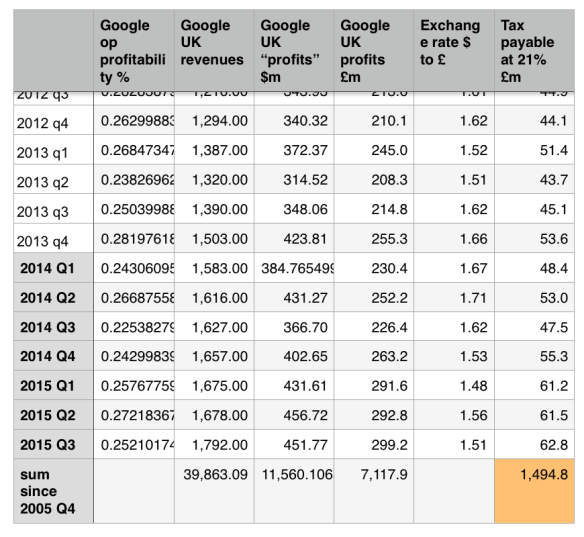

But let’s try anyway. Let’s use Google’s overall operating profit margin for each quarter, and use that to calculate the UK profits. It’s not perfect, but it’s a start.

I’ve done that in the table below, using the data from Google’s accounts, and its operating profit/revenue (hence operating profitability margin) to calculate a notional profit; then I’ve multiplied by the prevailing exchange rate (which has varied a lot over the years); and then I’ve multiplied the notional profit by 21% to get the “tax payable”.

The numbers are staggering. Google’s UK division has probably made profits of more than 7 billion pounds since the fourth quarter of 2005 (which I used simply because I couldn’t get exchange rates going further back) on revenues (stated) of $39bn – generating an assumed profit of $11.56bn, or £7.11bn.

And the tax payable on that amount? Assuming that same 21% rate as ITV, the total tax payable would be just short of £1.5bn.

And.. how much tax has Google paid in the UK?

The latest stories to emerge of the deal with HMRC suggest that Google is paying back tax to cover just that period to 2005.

“We have agreed with HMRC a new approach for our UK taxes and will pay £130m, covering taxes since 2005,” a Google spokesman said. “We will now pay tax based on revenue from UK-based advertisers, which reflects the size and scope of our UK business.”

How much tax has Google paid in the UK? A total of £200m if you include this latest £130m amount, apparently. Which works out to a tax payment rate of 2.8%. Sure, there may have been lots and lots of costs involved in setting up Google, which are offset against tax. But I doubt they’re bigger than ITV, for instance, has to pay.

Google’s deal with HMRC has been called “derisory”. The figures here suggest that that description is absolutely correct. If Google is generating this much revenue in the UK – a fact which it states in its earnings reports, for which its executives are legally liable – then it would be terrific if it could explain quite how it is so dramatically expensive to run such a business that it generates such pitiful profits. Update: the explanation given by tax experts is that the revenues are *generated* in the UK, but *booked* in Ireland, so that the “profit” arises in Ireland, which doesn’t tax it. This “generated in UK but booked in Ireland” point is the one which led to an almighty furore in 2013 when Matt Brittin of Google

stood by evidence he gave last year that all the company’s European sales were routed through its operation in Ireland and so were not liable to UK taxes.

To which the committee chairman, Margaret Hodge, responded:

“You are a company that says you do no evil and I think that you do do evil in that you use smoke and mirrors to avoid paying tax.”

Among the criticisms of the deal with HMRC are that it must have been done with some sort of principle in the minds of those who agreed the deal for HMRC – in which case it would be useful for other companies to know what principles exactly are in play. It’s time for transparency on this.

Nice work. Keep crunching the numbers Charles. This is the sort of evidence it will take to persuade people that Cameron, Osborne and co. and being taken for suckers.

When you have a few minutes spare, why not run the slide rule over Apple, Facebook, Microsoft, Amazon, Starbucks and other players of the double Dublin, Luxembourg gambit and other wheezes? Maybe that £1.5 billion would acquire and extra 0.

I’d definitely like to, but the problem with those is that they don’t give figures for the UK alone. However Apple looks to be on the hook for $8bn in back taxes (previously linked). Others too?

It’s an interesting exercise, but ignores the principles of arms length transactions and transfer pricing. Which change the picture completely.

Google US has ownership of a whizzy system that attracts traffic like there is no tomorrow. It can switch it on and off, like we saw with Google News in Spain.

http://arstechnica.com/tech-policy/2015/07/new-study-shows-spains-google-tax-has-been-a-disaster-for-publishers/

Now imagine that Google US was negotiating with a third party at arms length over licensing its whizzy system exclusively in the UK. What could they charge?

One option would be similar to the way the UK government auctions radio spectrum. The buyer would have to finance the enormous up front cost and service the debt out of future earnings.

Another option would be to negotiate a percentage-based licensing deal, which would be likely to be heavily loaded to Google US, because, well, it can do that. A rational UK firm in a competitive environment would rationally accept quite a small slice if it had no choice.

So you can see how in a genuinely arms-length arrangement (a pre-requisite for assessing fairness), the vast majority of the value is generated outside the UK.

Thanks, those are really good points. However, the fact remains that Google UK *isn’t* a franchise or a third party. It’s a subsidiary which is trusted to do all the things that the headquarters is, including Android development. In that way it’s not like McDonald’s or Starbucks; at some basic level we feel that there’s a key difference between monolithic companies like that, and the franchised ones (though the franchises don’t exactly get an easy ride).

The reality is still that one can’t feel that £200m is the best possible deal. If it were, Google would be fighting harder – as we’ve seen in the EC with antitrust, for example.

Without going into whatever devious structure Google might or might not have, it is *required* to account for transactions between group companies on an arms length basis, *as if* they were third parties… theoretically to reduce the possibility of artificially channeling profits to a low-tax area.

It has long been possible for HMRC to look through what they or the courts decide are artificial arrangements. But where you have an arrangement which has some business substance, that saves a disproportionate amount of tax, measures like the Diverted Profits Tax come in useful.

However, all settlements like that just achieved take into account a lot more than what a smell test (ignoring that ITV’s IP for leveraging the ad sales is almost exclusively developed in the UK, and Google’s is almost exclusively developed in the US) would dictate, eg. likely business restructuring by Google if a large penalty is demanded and a discount for the risk in attempting a formal case.

If HMRC had played hardball, Google could restructure to make collecting tax even harder, eg by loading debt on the UK subsidiary or taking an up-front licensing fee. That is why HMRC has to be pragmatic. There are arguments for limiting what debt servicing can be deducted from taxable revenue, in a more reasonable version of how buy to let landlords have just been raided, but I suspect that sort of legislation is even more problematic because of the vast knock-on effects.

Pingback: Start up: weather-forecasting phones, MPs v BT, Google’s UK tax row, Apple Street View?, and more | The Overspill: when there's more that I want to say

Pingback: Google £130m UK back-tax deal lambasted as ‘derisory’ by expert | Barking at cars