Remind you of the smartphone market? Red piranhas photo by Stig Nygaard on Flickr.

A friend of mine recently showed me his new handset. “It’s a Huawei,” he said. “Never heard of them, but it was a good price, and it does all I need.” He’d bought it to replace his ageing Nexus 4, and he seemed happy.

And so goes another example of Android dark matter: a company that is selling lots of handsets, but where we have no idea whether it’s making any money from them.

Yet we might guess that the answer is a qualified “no” when we look around at its rivals. Another quarter, and the profit story remains much the same: Apple and Samsung are making it all. The others whose financials we can actually see – LG, Sony, HTC, Lenovo, Microsoft, BlackBerry – all lost money as though it was what you’re meant to do. The big mystery: Huawei, which was the third biggest smartphone maker in this period, but doesn’t release financials. Is it making money? If so, it’s the only Android OEM besides Samsung which is to any notable extent.

But the third quarter, from June to the end of September (already receding into the distance) is notable because we’re now seeing the effect we’d expect from the rapid expansion of the Android OEM business: price deflation. It’s becoming rampant, and it’s beginning to tear into Samsung, which is being eaten from below by piranhas.

The effect of this was that even though Samsung shipped more smartphones than it has ever done before – a titanic 84.5m – its mobile revenues were only its 9th largest, and its mobile profits only one-third the size of its biggest (which came in early 2013).

That equally raises a very important question for the future of the big noise in the smartphone business: Apple. If even the biggest Android OEM is having its prices yanked down by smaller but numerous rivals, how (or how long) can Apple maintain its gigantic difference in pricing compared to those rivals?

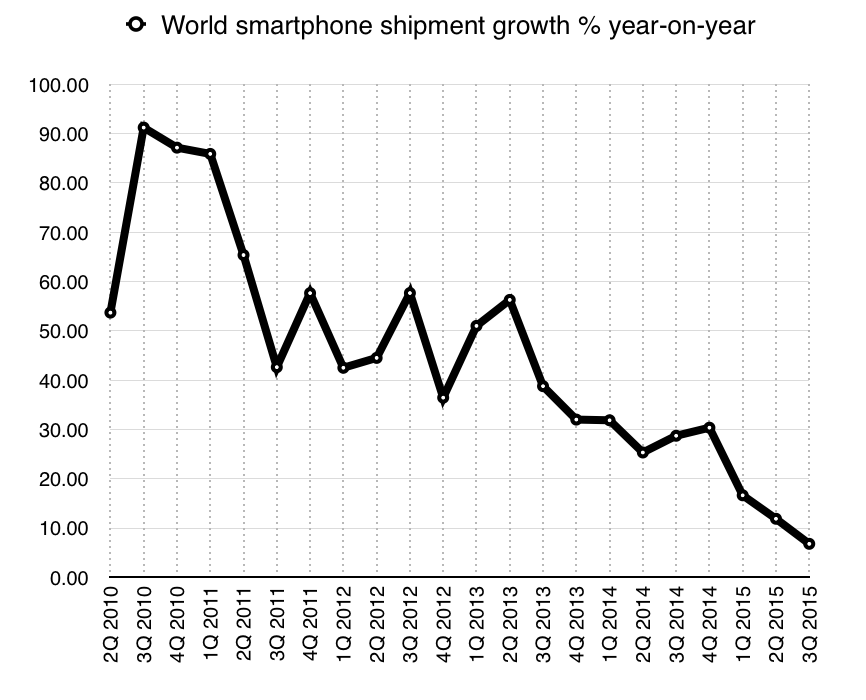

Note too that the smartphone market is still decelerating; from 11.9% growth (compared to the same period in 2014) in the second quarter, to 6.8% in the third, according to IDC’s numbers, which are the ones I use for consistency. (Gartner has a higher growth rate.)

Data from IDC

Score that

I’ve added two columns to the scorecard this quarter: year-on-year shipment growth, and that growth normalised against the whole smartphone market. Apologies if this demands a lot of horizontal scrolling.

| OEM | S/phone revenue US$ (approx) | Op profit US$m | Op margin % | S/phones shipped | Implied ASP per s/phone | Implied profit per s/phone | Shipment growth y/y | Shipment growth v s/phone mkt (6.8%) |

| HTC | $0.674bn | -$154m | –23.1% | 2.6m | $259.27 | –$59.85 | –46.9% | –53.7% |

| Sony | $2.32bn | -$171.7m | –7.4% | 6.7m | $346.12 | –$25.62 | –32.3% | –39.1% |

| LG | $2.96bn | –$88.6m | –2.3% | 14.9m | $198.49 | –$5.95 | –11.3% | –18.1% |

| Samsung | $20.70bn* | $2,440m | 11.79% | 84.5m | $248.55 | $28.86 | +7.6% | +0.9% |

| Lenovo (inc Motorola) |

$2.37bn* | -$217m | –9.2% | 18.8m | $126.22 | –$11.54 | –32.9% | –39.6% |

| Total for ‘public’ Android | $29.024bn | $1,810m | 6.2% | 127.5m | $227.64 | $14.20 | –7.7% | –14.5% |

| Huawei | ????? | ????? | ????? | 26.5m | ????? | ????? | +57.7% | +50.9% |

| Xiaomi | ????? | ????? | ????? | 18.3m | ????? | ????? | +1.1% | –5.7% |

| ZTE | ????? | ????? | ????? | 16.2m | ????? | ????? | +42.1% | +35.3% |

| Total for “dark Android” | ????? | ????? | ????? | 61.0m | ????? | ????? | +35.6% | +28.8% |

| Apple | $32.21bn | $9,022m* | (28% est) | 48.05m | $670.38 | $187.76* | +22.6% | +15.8% |

| Microsoft Mobile | $0.72bn* | –$603m | –83.8%% | 5.8m | $105.00 | –$104.00 | –38.6% | –45.4% |

| BlackBerry | $0.20bn | –$180m* | –89% | 0.83m | $242.16 | –217.00 | –61.9% | –68.7% |

* estimated smartphone revenues/profits/ASP only – excluding featurephones and tablets.

Working assumptions:

HTC: all revenues from smartphones – zero from the Nexus 9 tablet (pretty certainly true), zero from the HTC Re camera (probably true).

Sony: all revenues and profits from smartphones; zero from tablets – of which it shifted fewer than 1.6m, given IDC’s numbers; and zero profit from tablets. If tablets generated significant revenue and were profitable, then the smartphone ASP goes down, as does per-handset profit. (If tablets lost money, the per-handset loss is less.)

LG: $100 average selling price for the 1.6m tablets I’m estimating it shifted in the quarter. (That would put it equal with shipments in the previous quarter.) Tablets assumed to have zero profit, though they might have made some loss that made everything else look worse.

Samsung: featurephones (it shipped 20.5m) sold for $15, zero profit; tablets (8.0m) sold for $175 at zero profit. If the tablets or featurephones made any profit, then the profit from smartphones were lower.

Lenovo: assuming the 3.1m tablets it sold had an ASP of $100, and zero operating profit. If the tablet ASP was lower, Lenovo smartphone revenues were higher; if the tablets were profitable, per-smartphone loss was greater.

Apple: operating margin, as previously, of 28%. You could halve this, or even put it level with Samsung’s declared margin, and its operating profit would still be more than all the others’ profits (even ignoring losses) put together.

Microsoft Mobile: the figures here have to be backed out from the not-quite-stated phone revenue, including featurephones: “phone revenue decreased 58% by $1.5bn”, which takes us down to $1.1bn. There’s no gross margin given for phones, so I assumed –$104m, as in the previous quarter. Microsoft shipped 25.5m featurephones (up from 19.4m the quarter before, but down from 42.9m the year before) and 5.8m Lumia smartphones (stated; down from 8.4m the quarter before, and 9.4m the year before). Assuming featurephones had an ASP of $15 and made zero profit (same as with Samsung). The Lumia ASP has to be estimated, but seems reasonable.

BlackBerry: device revenue is given in financial statement; assuming software/services have gross margins of 84.5% (true historically), and that hardware R+D and sales costs are proportional to device revenues as % of overall revenues.

Troubles in common

Here’s the surprise: a number of Android OEMs managed to make their device ASPs rise from the previous quarter. First is Sony – up from $319.40 to $346.12. And who knows whether the $5m spent on product placement for Sony smartphones in the James Bond film Spectre won’t pay off some time. (They’ll have to have a hell of a return on investment, though.) HTC also managed it: up from $236.90 to $259.27. Lenovo also did it, up from $115.06 to $126.22.

And what else did those three companies, along with LG, all do? Lost money. The problem for premium Android goes on. We’re seeing the rise of “dark Android” – the companies which have huge reach (especially inside China) but whose finances are opaque. (All three of Huawei, ZTE and Xiaomi sell many, if not a majority, of their phones without Google’s services installed, because they sell them inside China.) Meanwhile Apple raises its ASP, and its profit rises in line, as far as we can tell.

The really interesting case is Samsung. A year ago, in the third quarter of 2014, Samsung had a terrible time: profits crashed and its semiconductor division became the most profitable part of the business – which is still the case. At that time, Samsung discovered that making a new “S” series phone wasn’t a guarantee of success; it was caught with lots of unsold Galaxy S5s sitting with wholesalers, and had to offer all sorts of discounts to get them moving, which hurt profits.

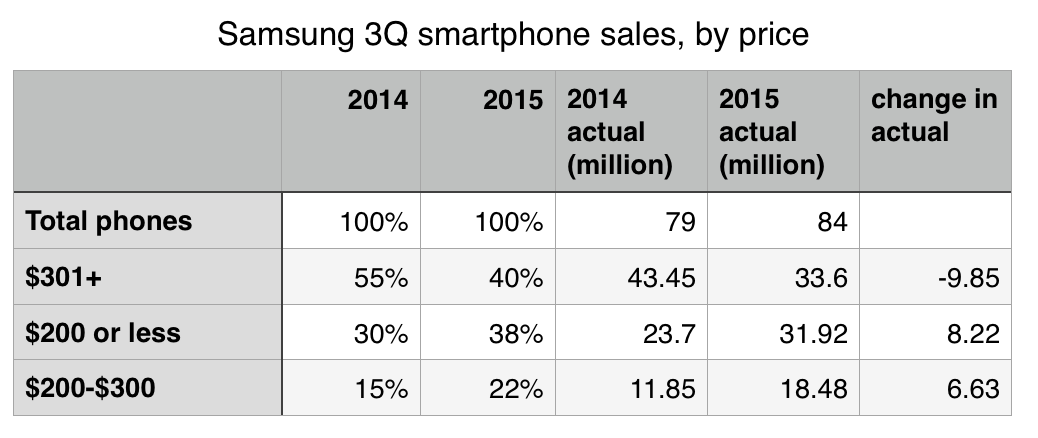

This time around, Samsung’s profits have risen year-on-year, but only because the same time last year it was so dire. The Wall Street Journal had some interesting data about how it managed to get so many phones sold: basically, it concentrated on the low-to-mid end. Screw the S6 and S6 Edge and its kin; this was about getting phones out the door.

…while 55% of its smartphones were priced at $301 per unit or more at this time last year, that high-end segment has fallen to just 40% of Samsung’s overall smartphone sales, Counterpoint said.

Phones priced $200 or below now account for 38% of total units shipped at Samsung, versus 30% this time last year.

You can work this out pretty easily:

Data from Counterpoint Research for 3Q 14 and 3Q 15

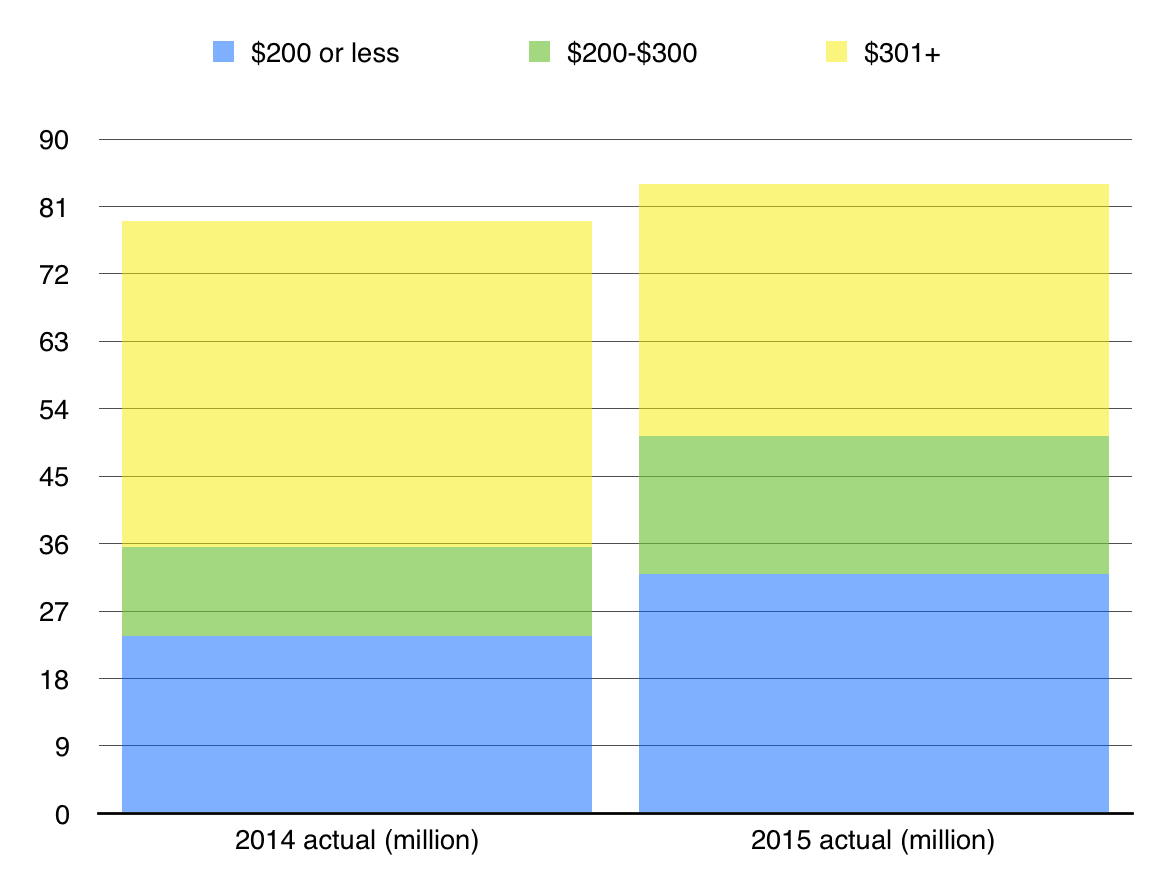

Here’s how that looks when you visualise it:

Data from Counterpoint Research. The mid-level segment is growing at the expense of the high-end one.

Look at how the blue and green edge up into the pricier yellow – which is now much smaller. And we’re comparing, remember, with last year, where the yellow (pricey) segment went pretty badly for Samsung as it was.

This is Samsung reacting to what’s going on in the market, and responding as it does best: by using its manufacturing and distribution might to try to squash competition. But in places like China and India, for example, local suppliers can compete pretty evenly:

“Samsung Electronics has decided to release the products priced at some 100,000 won for price competitiveness with Chinese and Indian smartphone makers. Local manufacturers, such as Xiaomi and Micromax, have already launched many models in the same price range. An official from the industry said, “Now, it is impossible to hold a dominant position in the competition just with a brand image of Samsung Electronics without releasing models in the same price range with local companies. When we have similar price competitiveness, we can defend our market share but profitability will get worse further.”

And LG? It’s getting walloped. Strategy Analytics says (in a super-pricey report I won’t buy) “LG’s global handset shipments dipped -21% YoY in Q3 2015. Competition from ZTE, Huawei and others ramped up across Asia and North America. A major challenge for LG is that it still has too many eggs in too few country baskets and it badly needs to diversify geographically for regrowth in 2016.”

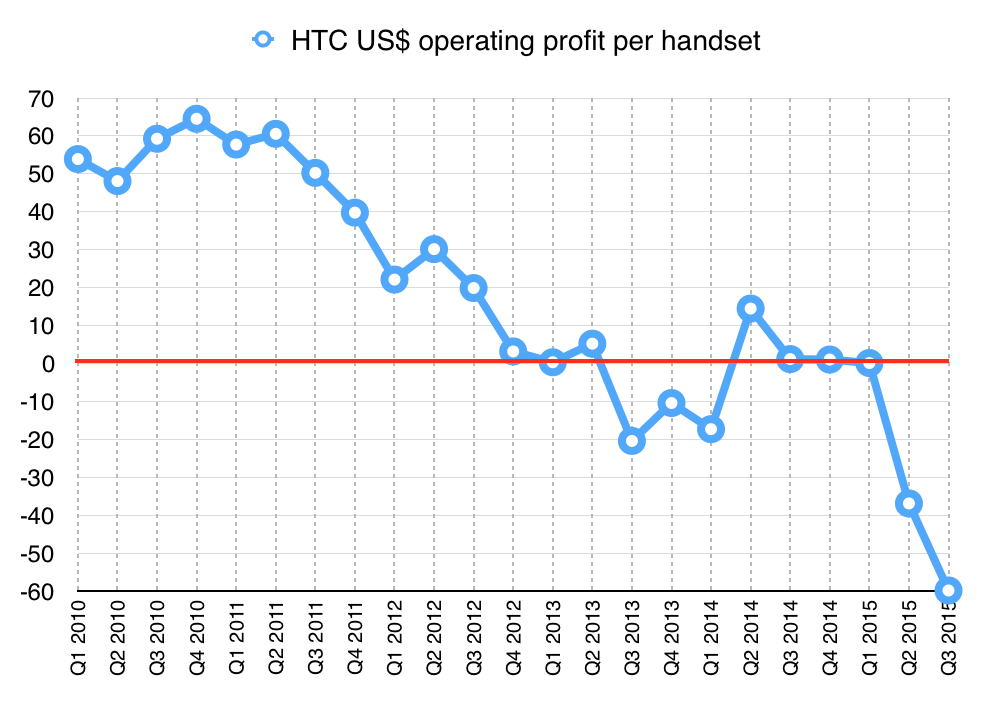

I don’t see that happening. What I find remarkable is that top-end Android vendors are now howling into the hurricane. The LG G4 has a camera that seems remarkable in all the sample shots I’ve seen; yet it’s struggling to sell them. HTC might hope that the newly released iPhone-alike A9 will raise revenues briefly this quarter, but I’m pretty sure they won’t reverse its per-handset losses, which are looking awful:

Data calculated from HTC financials

Android’s dark matter

Consumers are clearly beginning to think that many other Android handsets are “good enough”. My friend with his cheap Huawei handset is just one example. ZTE and Xiaomi and OnePlus and, now, the UK’s WileyFox and Marshall (the amplifier makers, yes) and even Pepsi are all piling into the handset market, sure that they can make money.

In some cases, it’s quite possible they are: by restricting its supply and distribution, OnePlus has a model that can scale as long as it can keep a lid on demand. What the phone OEMs really want is to be able to move closer to a Dell-type model: where you order the device and it’s pretty much custom-made for you from modular parts. That means lower inventory, and certainty about pricing components and satisfying demand.

Meanwhile, Android OEMs such as LG, Sony and Samsung are faced with the harsh reality spelt out by Ben Bajarin in one of his columns:

as a market matures, the early innovators get disrupted by competitors who come into their space with lower priced products, similar specs (the specs that matter), and eat into the market share of the early innovator in the category. Once the market embraces “good enough” products, the innovator can no longer push premium innovations as their value is diminished once a “good enough” mentality sets in. Android devices in the $200-$400 range are “good enough” for the masses, leaving Samsung’s $600 devices and above stranded on an island.

As he points out:

the innovator’s dilemma, in this case, only applies to Android-land because all the hardware OEMs run the same operating system. As I’m fond of saying, when you ship the same operating system as your competition you are only as good as their lowest price.

This is what Samsung is reacting to, but Sony and LG and HTC can’t react to without cutting their own throats even more. They have high fixed costs in order to produce those super-high-resolution phones (QuadHD, anyone? Even if you can’t tell the difference?) but it doesn’t cut any ice with the public.

Meanwhile Huawei, ZTE and Xiaomi the dark matter of the smartphone business: we know they’re there because of the enormous influence they wield on everyone around them. They’re also the only part of the Android OEM business that’s growing. But it’s very hard to have any idea of their financial position. (You can get some idea: CoolPad says it can’t make sufficient profit to sell a tablet to compete with Xiaomi’s newest model at the same price.) The way that the low-price piranhas are piling into Android does remind me of the days when the iTunes Music Store was taking off, and every company in a vaguely associated area scrambled to have their own download store – HMV, Tesco, Wal-Mart, Virgin – without much consideration of how they’d turn it profitable; they just reckoned it was a good idea. (Most have now shuttered those stores.)

In the same way, offering an Android phone is beginning to look like a possible sideline for all sorts of companies, which speaks to the problem that the big Android players have: if anyone can make a smartphone, why are they making a smartphone? Sure, the rivals don’t outsell the big players, but they don’t need to. For almost any price, control your inventory and demand and you control your profitability.

Black days for BlackBerry

You’ll notice BlackBerry’s figure, where its costs are so mad that it’s effectively losing enormous amounts on each device it sells. Chief executive John Chen may say handsets are “profitable”, but that’s gross margin, before you take away distribution, administration, sales, and R+D. In day-to-day terms, BlackBerry’s hardware division is a mess, and I don’t see why Chen doesn’t say “we’re going to go into a maintenance mode where we supply legacy handsets to existing clients on demand” and simply focus on the software/services business for profit. The BlackBerry Priv would have to be a colossal hit to make up this ground, and there is simply no sign of that happening. Richard Windsor agrees:

The new BlackBerry Priv and its rumoured successors are aimed at such a narrow niche that I doubt that they will ever make money. Once this realisation has sunk in, I think that BlackBerry will abandon its hardware business and focus on its software business which has recently been bolstered with the acquisition of Good Technology.

The iPhone pricing puzzle and the single spec that matters

How much longer can Apple keep on with its premium pricing? This question has been asked pretty much since the first Macintosh was launched. The answer from the PC market seems to be “a lot longer than you might expect”. In the smartphone market, the distance between the iPhone ASP and the average Android handset ASP, even on these public figures, is $450, which is itself double the price of the average Android ASP. And it’s unlikely that the missing Android data covers handsets with higher prices.

This seems like a situation that can’t last, and yet we’ve seen in the PC market that it can and does: Apple’s ASP there is over $1,200, while that of the big five Windows PC makers wobbles around $500. Apple also makes about twice the operating profit on PCs as HP, Lenovo, Asus and Acer combined.

Yet in a space where prices of phones are dropping precipitously, the iPhone’s price tag seems more and more anomalous. Yet by standing outside those price wars, and by incrementally improving its offering again and again, it keeps pulling it off. In part, that’s because of the price: as CCS Insight noted in April,

Apple’s success in opening up new, high-growth markets such as China, India and Indonesia is significant. Although its products are out of reach for many people, the iPhone is widely regarded as a badge of success in these countries and there are still enough buyers who are affluent enough to afford one.

In that sense, the price is a spec – one where rivals are actually being degraded. It sounds completely contrary, but to a number of people an iPhone is an affordable luxury. Think of it like a car: some people really want Porsches. But if you could buy a Porsche for the same price as any other car, would it still have that cachet?

Maturity and change

We’re now moving into a situation where the biggest markets – China and the US – are approaching saturation, so that it becomes increasingly hard to persuade the remaining featurephone owners to trade up, and people are less willing to buy a new device just because it’s new. That CCS Insight forecast in April also says that smartphone sales in western Europe and North America will peak in 2017; but it also expects Apple’s share to grow.

Again, this seems contrary – won’t that just lead to people being driven by price? But in a mature market, you can get a move towards perceived quality and luxury, because you’re in a situation of plenty. As I showed using Ericsson’s data from mature markets, Apple can gain users in that situation, creaming them off from Android (and to a less extent from Windows Phone).

Conclusion: segue to VR

Three months or so back I wrote about “premium Android” hitting the wall. Now it’s sliding down, and being swallowed by dark matter and eaten by piranhas. So what keeps the lossmaking companies in the business? I think it’s pretty evident that they now have their eyes on the future: virtual reality. It’s a hugely promising technology which demands integrated systems with gyroscopes and, moreover, super-high-quality screens where you can’t discern pixels even if it’s a few inches from your face. That’s what Sony, LG, HTC and Samsung are all aiming at; each has its own offering in VR, while Apple hasn’t so far made a move.

Perhaps, though, history is going to repeat itself here. Each of those companies was strong in phones before Apple came onto the scene with the iPhone. It cannot have escaped Apple’s notice that VR is a promising market, with lots of applications. And it has been granted patents in that space.

Maybe in a few years’ time, we’ll be scoring profits in the VR market. For now, though, it’s all about smartphones – and there are still only two clear winners.

More articles to read:

• BlackBerry might have no BB7 users left by February 2016

• Premium Android hits the wall: the Q2 2015 smartphone scorecard

• Google’s growing problem: 50% of people do zero searches per day on mobile

• The adblocking revolution, and iOS 9

Pingback: Dark matter full of piranhas: Android, Apple and the 3Q 15 smartphone scorecard | tightlinesandsunshine

Pingback: Virtual Reality: Welche VR-Brille setzt sich durch?

Pingback: SEO ist tot - juliancordes.de