Lenovo’s Yoga Android tablet: likely not much profit here. Photo by pestoverde on Flickr.

Corporate reorganisations! What are they good for? Absolutely nothing – except in the rare cases when they force a company to restate its financial results using the new reporting lines. The fallout from this is that you can often figure out, at least for a few previous quarters, how previously hidden bits of the company were faring.

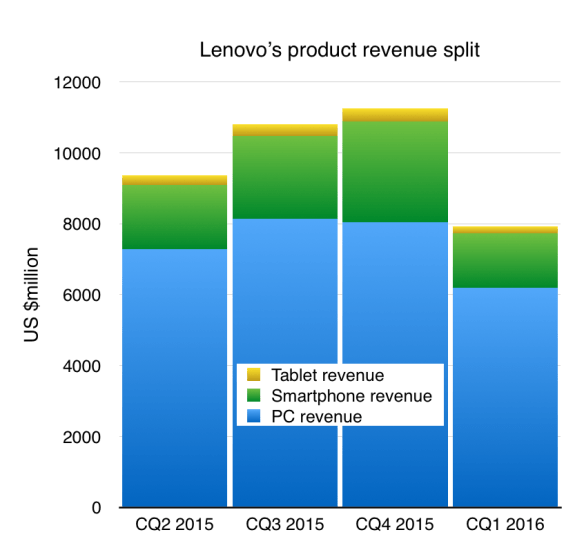

Which leads us to Lenovo, which in April reorganised itself from having a “PC” division which made PCs, and a “mobile” division which offered smartphones and tablets, to having a “PC and smart devices” group which offers PCs and tablets, and a “mobile” group which offers smartphones.

It restated its revenues and operating profits for those divisions for the previous four quarters. What happens when it does that is that you can see, by how the numbers shift, what sort of contribution tablets were making to the overall business.

Reshape, restate

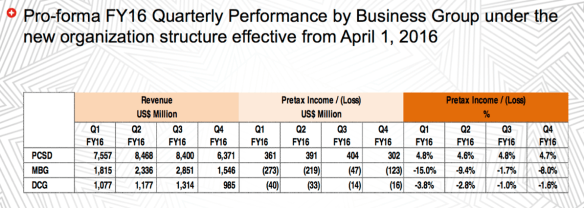

The results for the April-June quarter (the calendar Q2, but Lenovo’s fiscal Q1) include this restatement:

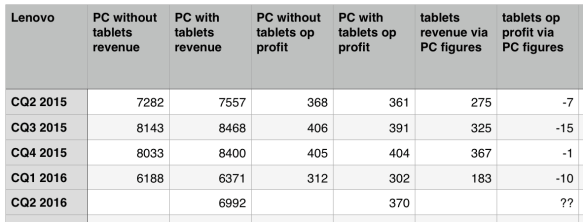

Of course the old numbers for the previous organisation are still there. So to find out how much business, and how much profit, we just go back and compare the old numbers with the new ones – that is, the PC-only figures for revenue and operating profit, and the PC-plus-tablet figures.

A quick bit of arithmetic then shows you the tablet revenues and operating profit.

(Note this is only the Android tablets – the Windows devices were already part of the PC division.)

Here’s what we get.

(“CQ” means “calendar quarter”, eg CQ1 is January-March.)

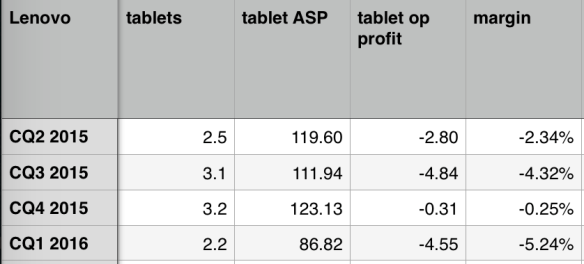

And as IDC records tablet shipment figures, we can also get the per-tablet average selling price (ASP) and per-tablet profit.

The raw figures for ASP, profitability and volume are these:

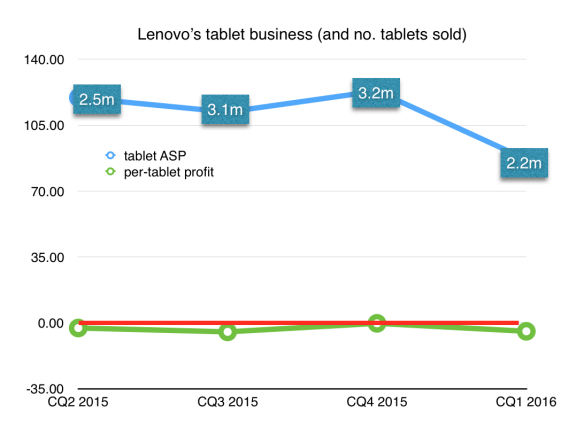

Which make this graph:

(figures in US$)

A bad business

What have we learnt? It’s long been fairly clear that Android tablets really aren’t a great business to be in. They’re low-volume, low-margin (if there’s any margin at all) and because it’s Android, people tend to have little brand loyalty – essentially, it’s a glorified screen.

I can’t see that any of the smaller competitors in Android tablets (Acer, Asus, Lenovo, Huawei, LG) are making an operating profit, or at least one worth considering. Sure, they will make gross profit – they get more money than the raw materials cost – but once you include other costs such as sales, marketing, administration and R&D, they’re sunk.

Samsung is the exception here: I’m confident its tablet business is profitable, because it has scale (it’s the largest Android tablet maker by some distance, with 6m shipped in the second quarter, making up about 25% of all Android tablet shipments) and also makes the components itself; that flywheel effect of creating your own scale with stuff you make yourself has a knock-on effect. But even Samsung has struggled with the idea of high-priced tablets; it has considered just giving them up and aiming for the low end. But it didn’t.

The lower you go

Looking at Lenovo’s ASPs, which wander around the $110 mark (I’ve previously guessed them at $100 and zero profit in my handset analysis; nice to have that confirmed), it’s easy to see why. There’s barely any money in Android tablets – a fact that was confirmed after I wrote this post (see the update at the end). Take a look at how small a part of Lenovo’s business they are:

In his meta-analysis of the Android-iOS landscape, Benedict Evans estimated that there are 150m-200m Google Android tablets in use, and perhaps another 200m “naked Android” (no Google services) in China. For comparison, he reckons there are about 250m active iPads, of varying sizes.

The key difference is that Apple’s iPad sells for way more than Lenovo’s (or Samsung’s). The ASP for all iPads in the latest quarter was $490, and it has never fallen below $400. Sure, you can argue that the iPad is overpriced, but you can also expect that as long as it keeps selling, Apple will get the profit it needs to encourage it to keep going.

The other point: if you can can’t make a profit selling tablets, you won’t be able to improve them, or market them seriously.

Compare that with Apple’s efforts, where its True Tone screen (on the 9.7in iPad Pro) is likely – certain, really – to come to the new iPhones later this year. But in the tablets first. Lenovo can push – but only because it has the PC division. The tablets, have been dragging it down.

And finally..

There’s a nice coda. In its latest results, Lenovo says “Tablet: profitable with double-digit growth premium to the market”. Looking back, it has never before said that tablets were profitable; it’s done lots of talking about growth and position, but not profit. We can’t see how profitable, though, because we don’t have those comparative numbers as we did before.

The other coda: you can work out the tablet revenues and profits by using the pre- and post-split numbers from the smartphone division. But they come out different. Via the smartphone division, revenues come out as $1,231m v $1,150m via the PC division; operating profit comes out as -662m from the smartphone numbers, v -33m from the PC numbers. But I’ve gone with the PC figures, because there are all sorts of writeoffs – inventory, restructuring, redundancy, acquisition of Motorola – in the smartphone numbers which confuse things hugely. There are no such in the PC division numbers, so I’ve gone with them.

(Update: corrected typo of “if you can’t make a profit selling tablets..”)

Bigger update: a week after this appeared, Digitimes had two stories on the squeeze in the tablet market. The first noted that in 2Q 2016, the tablet market shrank again, to 40m units:

Among the three major camps [Apple, brand OEMs and cheap “white box” vendors], white box players performed the weakest in the second quarter. With more large-size independent design houses (IDH) quitting the market plus shortages of components including panels, memory and processors, white-box players saw their combined shipments drop to a new low at 13.8m units in the second quarter.

Non-Apple first-tier vendors’ inexpensive tablets were mostly released in the second quarter, but combined shipments were down 7.1% sequentially to reach only 16.98m units as product differentiation, number of models, and price competitiveness were all inferior to in 2015.

And then there was the news you might expect, of both brand names and white box vendors pulling out:

Asustek Computer and Acer have turned to focus more on niche applications, while Micro-Start International (MSI) has already phased out of the business and to focus mainly on gaming PC product lines. China-based white-box players that have joined Intel’s China Technology Ecosystem (CTE), have also mostly stopped pushing tablet products.

Dropping demand is expected to cause Asustek’s tablet shipments to fall below three million units in 2016, according to sources from the upstream supply chain, leaving Apple the only player that is still able to achieve strong profits from the tablet sector.

That’s pretty stark. (Note that the Digitimes stories go behind a paywall after a few days, if you’re coming to this late.)

Asus, you’ll recall, made the Nexus 7, which was probably the best-selling Android tablet ever – Sameer Singh estimated it at around 6m-8m units in 2012.

But a lot of the companies that jumped into the market thought that tablets would be like smartphones – updated every year, or perhaps every two. Turned out they were all wrong, including Apple; the sales cycle looks more like three or even four years, much closer to a PC. (The iPad 2, from 2011, is still widely used.) After the boom in 2012, the tablet bust has been abrupt – and only those with the manufacturing and financial muscle have been able to stay the course.